Tue Jul 16 2024

Annual Percentage Rate (APR) vs Annual Percentage Yield (APY)

APR and APY sound similar, so many people get them mixed up. Here’s what each term means and when to use it.

FDIC-Insured - Backed by the full faith and credit of the U.S. Government

Author: Richard Horowitz

September 12, 2025

People talk about inflation and interest rates all the time, but understanding the relationship between them is the most important piece of the puzzle.

The two forces of inflation and interest rates shape everything in finances, from the cost of borrowing to the value of your savings. When inflation rises, interest rates often follow, and vice versa. This push and pull can influence the entire economy, from national policy to your everyday purchases.

That’s why learning about inflation and interest rates is a vital and valuable part of financial literacy. It helps you better manage debt, build credit, and prepare for future financial shifts.

Inflation is a measure of the rate at which prices for goods and services increase over a defined period of time — typically one year. It reduces the purchasing power of money, meaning that what costs $1 today may cost more next year, and potentially even more the year after that. You can look at inflation rates for specific kinds of goods, as well as the overall economy.

If inflation is high, it means prices are increasing quickly. And low inflation means a slower price increase. If prices actually go down instead of up, we call that deflation.

Inflation can make everyday items more expensive for each of us. But it can also have larger community impacts, leading to increased costs for housing, transportation, and services. Governments may even struggle with budget pressures and rising debt. Understanding inflation helps consumers and policymakers adapt to a changing economic landscape.

The Core Personal Consumption Expenditures (PCE) Index tracks the price of specific consumer goods and services, excluding food and energy because of their pricing volatility. The Federal Reserve (the Fed) prefers this metric for gauging long-term inflation trends.

Because it reflects consumer behavior and pricing in a more stable way, the Core PCE helps the Fed make decisions on interest rates and monetary policy. A rising Core PCE typically signals inflationary pressure that could prompt action from the Fed.

Interest rates show us the amount it costs to borrow money. For consumers, this directly impacts things like credit cards, loans, and mortgages, typically as an annual percentage rate (APR).

Inflation is just one of several factors that can impact interest rates. Economic growth, central bank policy, and market demand all play a role, too.

When rates are high, borrowing money becomes more expensive, which can curb spending. When they’re low, borrowing and investing are more attractive for consumers.

When choosing a credit card, it’s crucial to compare interest rates to avoid costly debt. You’ll also want to evaluate perks, so you can find a card that maximizes rewards. Of course, it’s not just credit cards — it’s important to compare interest rates when looking for any kind of loan, including auto loans, student loans and mortgages.

During recessions, economic activity slows, and people tend to spend less. To stimulate growth, the Fed often lowers interest rates. Cheaper borrowing encourages spending and investment, which can help jumpstart the economy.

For consumers, lower rates can reduce monthly payments on variable loans and credit cards. Historically, recession-era rate cuts aim to make credit more accessible and support job creation and business expansion.

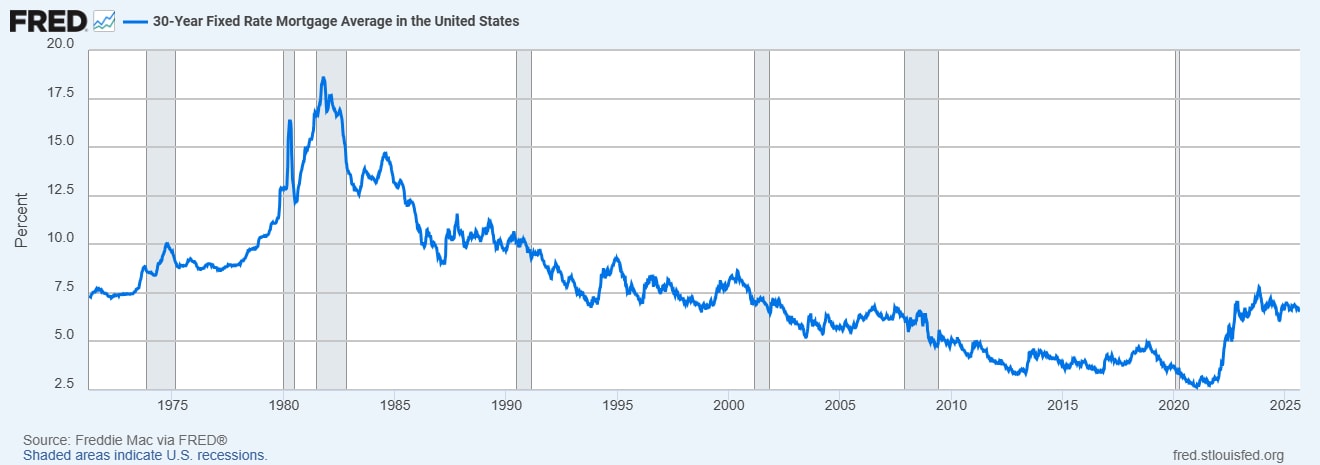

Interest rates have fluctuated significantly since the Federal Reserve started tracking them in 1954. This is how mortgage rates have changed over time:

Image Source: https://fred.stlouisfed.org/series/MORTGAGE30US

Interest rates can be used to help control inflation. For instance, if inflation is too high, the Fed may raise interest rates in an effort to slow down borrowing and spending. This increases the cost of loans and credit, which tends to reduce consumer demand for loans.

With less money circulating, businesses may hold off on raising the prices of their products and services. In turn, this can bring inflation under control.

However, low interest rates aren’t always beneficial. When interest rates are too low, they can actually overstimulate the economy and increase the risk of inflation.

When inflation rises, lenders often charge higher interest rates to compensate for the loss of purchasing power over time. And then the Fed may respond by raising overall interest rates to cool the economy and prevent further inflation.

Inflation expectations also influence investor behavior in the bond market, which affects lending rates. Essentially, persistent inflation means money is losing value, so both markets and central banks adjust interest rates to prevent prices from rising too rapidly. This helps maintain overall economic balance.

The Federal Reserve raises interest rates primarily to curb inflation and stabilize the economy. When spending and borrowing rise too quickly, it can push prices up. By increasing rates, the Fed makes credit more expensive, slowing down consumption and investment.

The Fed’s goal is to maintain price stability, support maximum employment, and ensure moderate long-term interest rates. These adjustments are part of the Fed’s monetary policy, designed to keep the economy healthy and balanced.

Inflation can impact virtually all goods and services you purchase. To maximize the value of your dollar in a fluctuating economy, it’s important to take some steps that can protect yourself and your wallet from inflation.

Here are some strategies to consider:

Understanding the connection between inflation and interest rates can help you make more informed financial decisions, whether you’re choosing a credit card, investing, or managing debt.

While these economic forces may seem complex, their impact on daily life is very real. By staying informed and taking proactive steps, you can better protect your financial well-being no matter how the economy shifts.

About the author:

Richard HorowitzRichard Horowitz is a contributor focused on the credit card and consumer financial services industry. As SVP of Marketing, he works on strategies related to customer acquisition, lifecycle engagement, and customer communications. Richard writes about topics including credit card usage, consumer credit behavior, and financial habits—such as how individuals use credit in everyday situations, what may impact credit scores, and broader trends in spending, saving, and managing credit.

This material is for informational purposes only and is not intended to replace the advice of a qualified tax advisor, attorney or financial advisor. Readers should consult with their own tax advisor, attorney or financial advisor with regard to their personal situations.

Tue Jul 16 2024

APR and APY sound similar, so many people get them mixed up. Here’s what each term means and when to use it.

Tue Aug 26 2025

Most of us like interest when earning it, but not when paying it. Some strategic financial moves will help you minimize or avoid these charges.

Mon Dec 04 2023

Inflation is an inevitability for any economy, so it’s important to prepare for it. One valuable tool for achieving this is portfolio diversification.