Tue Apr 07 2026

51% of U.S. Consumers Expect AI to Replace Financial Advisors

A new survey reveals how many U.S. consumers trust AI for financial advice — and why human advisors still hold an edge.

FDIC-Insured - Backed by the full faith and credit of the U.S. Government

June 10, 2026

Would you leave your money untouched for a fixed term if it meant earning a higher return? Here’s what U.S. consumers said about it.

In this article:

When uncertainty creeps into daily life, U.S. consumers tend to keep their money close by and liquid just in case they need it. But a growing body of evidence suggests that impulse may be costing them, even if it’s understandable.

A new survey of 1,000 U.S. adults commissioned by Credit One Bank reveals a striking tension at the heart of how consumers manage their savings: nearly half say they’d willingly lock money away for a guaranteed return, yet their biggest fear is they need it for an emergency and won’t be able to access it. This speaks to something deeper: anxiety about what tomorrow might bring.

That gap between intention and action is less about financial literacy and more about something deeper — like anxiety about what tomorrow might bring.

For many U.S consumers, assessing their personal savings can be stressful. Women report feeling anxious at nearly twice the rate of men. Lower-income earners describe their savings situation as “embarrassing.” And 1 in 3 U.S. consumers say they dip into savings every month — not for emergencies, but for everyday spending. The story these numbers tell may be more about who feels financially stable enough to think beyond next month than the rates and products themselves.

Nearly 52% of U.S. consumers say their biggest fear about locking up savings is losing access in an emergency, rising to more than 67% among 30–45 year olds

30% of U.S. consumers are “not confident at all” that they could cover a $50,000 unexpected expense without touching locked savings, climbing to almost 41% among those earning $25,000–$49,999

Among high earners ($100K–$249K), more than 25% say their top fear is locking in and watching rates rise, compared to just over 4% of those earning under $25K

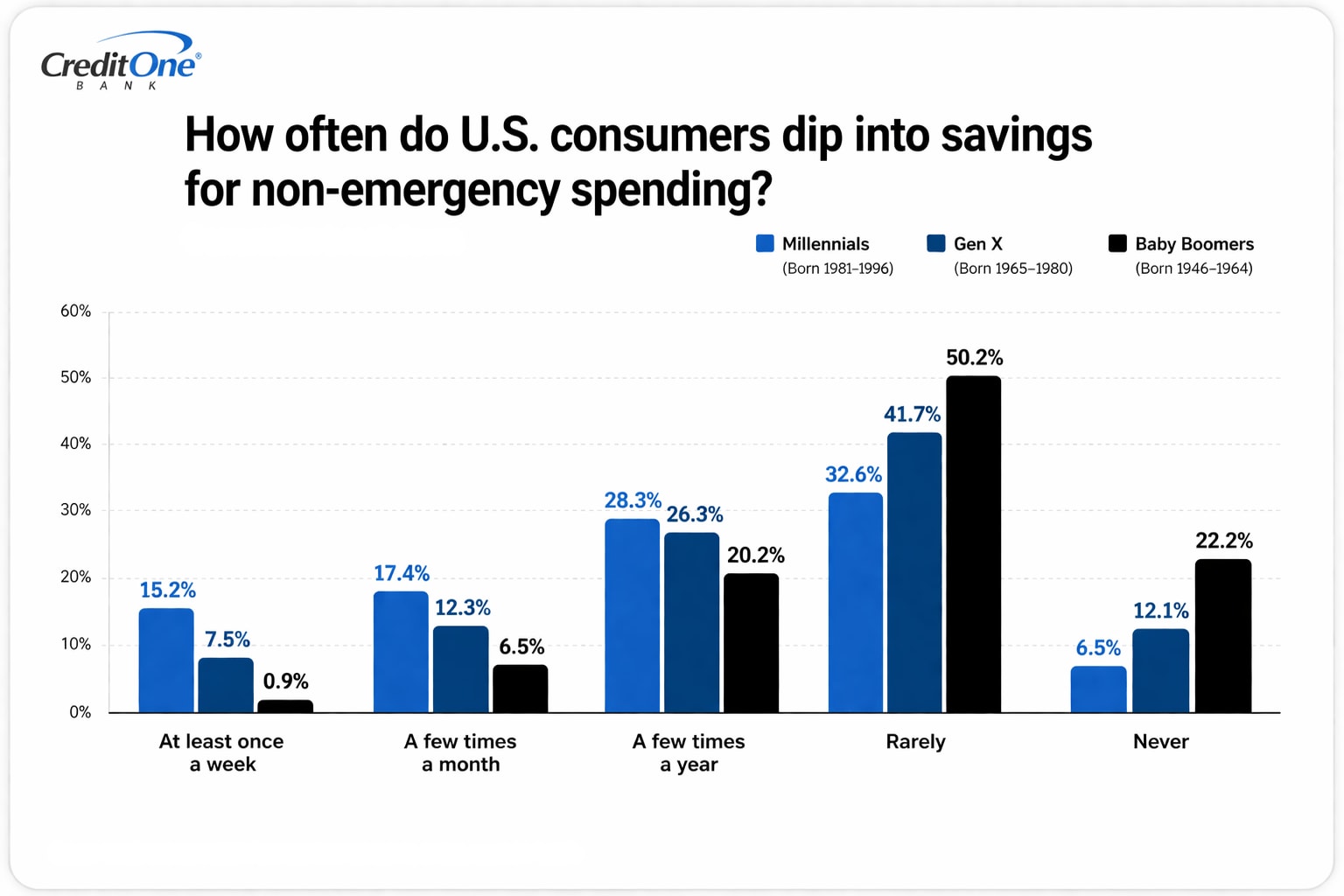

Almost 33% of 30–45 year olds dip into savings at least once a month for non-emergency spending, vs. just over 7% of those 62 and older

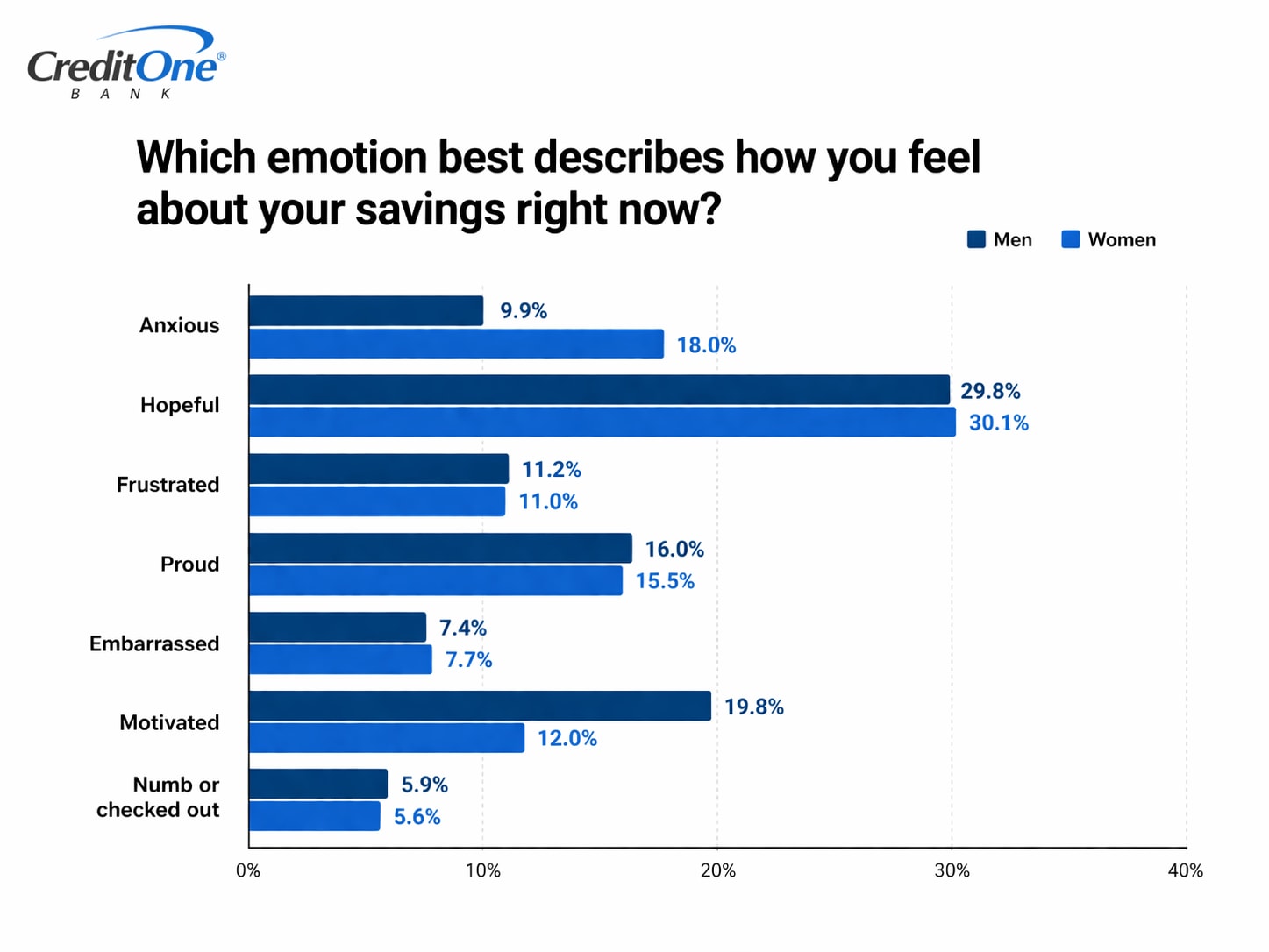

Women are nearly twice as likely as men to describe feeling anxious about their savings (18% vs. almost 10%)

More than 89% say they’d be more interested in locked savings if it included one penalty-free emergency withdrawal

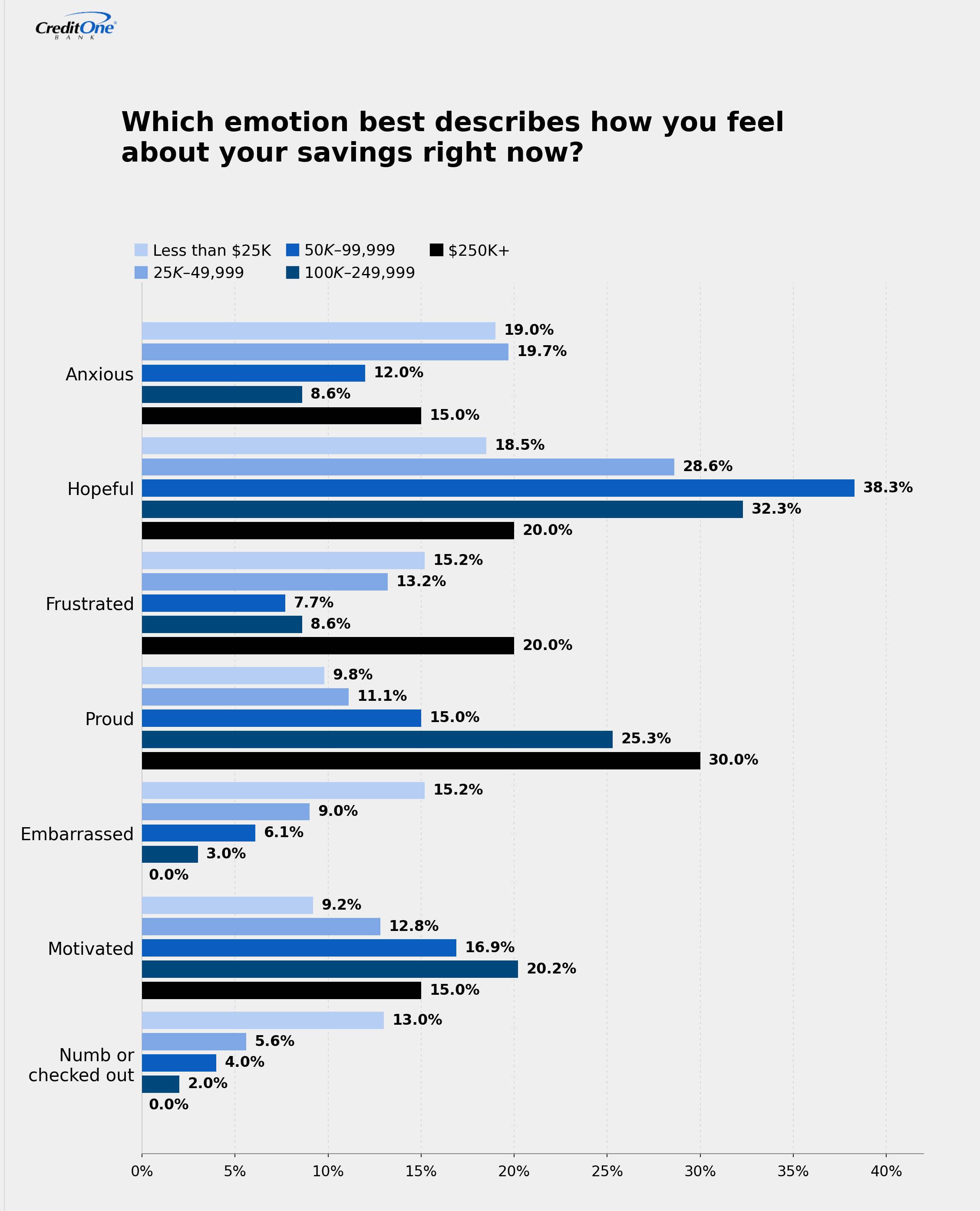

Over 15% of those earning under $25K describe their savings emotion as “embarrassed,” vs. just 3% of those earning $100K–$249K

Ask U.S. consumers why they don’t lock their money into a higher-yielding savings product, and the answer almost never starts with interest rates. It starts with a fear of the unknown.

More than half of survey respondents, nearly 52%, named losing emergency access as their single biggest concern about locked savings. That figure isn’t surprising on its own. What makes it striking is how sharply it climbs when you filter by age: among 30–45 year olds, it hits more than 67%. This is the demographic most likely to be managing mortgages, children, aging parents, and rising household costs simultaneously. For them, liquidity is more of a survival strategy than a preference.

That fear didn’t emerge in a vacuum. U.S. consumers who entered the workforce during the 2008 financial crisis spent formative years watching emergency funds vanish overnight. Financial planners responded by doubling down on the three-to-six month savings rule, and some people may have interpreted that to mean the focus should be on liquidity.

Add a pandemic and back-to-back inflation spikes on top of that, and keeping savings untouched, flexible, and within reach starts to feel less like caution and more like hard-earned wisdom.

Financial confidence isn’t evenly distributed in the United States, and this data makes that relatively clear.

When asked how confident they were in covering a $50,000 unexpected expense without tapping locked savings, nearly 1 in 3 U.S. consumers said “not confident at all.” For households earning between $25,000 and $49,999, that number climbs to almost 41%. These people simply may not always have the bandwidth to take on extra risk, even if it’s the relatively low risk of a fixed-term savings product.

This segment of the population may be rationally prioritizing survival over financial optimization. Keeping their savings close and available is a logical response to a financial environment that has repeatedly proven to be unpredictable.

The Federal Reserve’s own data seems to support this, although on a much smaller scale. In its most recent annual survey on household economic well-being, the Fed found that only 63% of U.S. adults said they would cover a hypothetical $400 emergency expense using cash or its equivalent, a figure that has declined from a high of 68% in 2021.

Here’s where the data gets interesting: the top-of-mind concerns for low-income households barely register for high earners, and vice versa.

Among U.S. consumers earning $100,000–$249,000, more than 25% say their biggest hesitation about locking in savings is rate risk: commit to a rate today, and then watch better rates emerge — unless you have a CD that lets you bump up your rate. That’s a legitimate, sophisticated concern, but it’s a concern you can only afford to have if emergency access isn’t already keeping you up at night.

For households earning under $25,000, rate anxiety affects just over 4% of respondents. Their concern is categorically different: will I be able to get this money if I need it? The contrast reveals two completely separate savings psychologies for similar financial products: High earners are optimizing while lower earners are protecting. Product designers and financial educators who treat these groups as one audience are speaking a language that only half the room understands.

The 2022–2023 rate hike cycle made this split vivid in real time. The Fed raised rates 11 times between 2022 and 2023, pushing top CD yields past 5%, which is the highest level in over a decade. Savers who had locked into a one-year CD at 0.13% to 0.25% APY in early 2022 watched rates climb up to 40 times higher within 18 months.

For higher earners paying close attention to yield, the memory of locking in too early is exactly the kind of lesson that sticks. For lower earners, that entire conversation was beside the point, as access to the money mattered far more than what it was earning.

Millennials aren’t just hesitant to lock up savings. Many are even spending what they do have instead.

Nearly 33% of 30–45 year olds say they dip into savings at least once a month for non-emergency spending. Compare that to just over 7% of U.S. consumers 62 and older, and the generational gap becomes a chasm.

To be fair, this millennial demographic may be facing a unique combination of financial pressures like student debt, childcare costs, and housing prices that have outpaced wage growth for over a decade. Monthly savings withdrawals are often simply about the gap between income and expenses.

This behavioral pattern has a compounding effect, though. Each withdrawal erodes not just the balance, but the psychological sense of financial security. When savings feels precarious, the idea of locking it away, even for a better return, becomes almost unthinkable. It’s hard to plan for the future when the present keeps demanding attention.

The data from other sources reinforces the pattern. Millennials’ share of credit card balances surpassed baby boomers’ for the first time in 2023, according to TransUnion. This reflects a generation spending in a high-inflation, high-rate environment with steep consequences. Maybe even more so than previous generations. And with those conditions, the monthly savings withdrawal simply acts like a pressure valve.

The data on how men and women experience their financial situations is one of the more concerning findings in this survey.

Women are nearly twice as likely as men to describe their primary emotion around savings as anxiety: 18% vs. almost 10%. But when you stack up all the negative emotional responses — anxious, frustrated, embarrassed, numb — the gap lessens. Women hit 42% overall compared to 34% of men.

The implications extend beyond individual wellbeing. Emotionally charged financial environments tend to push people toward conservative, low-return behaviors like keeping cash in checking accounts, avoiding investment products, and resisting any structure that feels like loss of control. The anxiety itself becomes a barrier to better financial outcomes, creating a cycle that’s difficult to break without addressing its emotional roots.

And those roots run deeper than psychology. Women often earn less over a lifetime, may take more career breaks for caregiving, and on average live longer than men, meaning their retirement savings need to stretch further with less to start.

Research from the Financial Health Network found that single women only have 40 cents for every dollar owned by single men, and that wealth gap compounds over time. When savings anxiety is twice as prevalent among women, it highlights a financial system that has historically given women less margin for error.

If there’s a single data point in this survey that financial institutions should take note of, it’s this one.

Just over 89% of U.S. consumers say they’d be more interested in a locked savings product if it came with one penalty-free emergency withdrawal. Among those respondents, more than 44% said they’d be “much more interested,” not marginally. Less than 7% said it wouldn’t make a difference.

This is a rare finding in consumer research: near-universal appeal for a single product feature. It suggests that the barrier to locked savings isn’t really about giving up access for a guaranteed return on a high-yield CD after all.

Instead, the barrier is structural. If we remove the one worst-case scenario (needing the money and facing a penalty), then the product becomes dramatically more attractive across nearly every demographic group.

Money shame is real, and it tends to track pretty closely with income.

Among U.S. consumers earning under $25,000 per year, more than 15% describe their savings situation with the word “embarrassed.” That number drops to just 3% among those earning $100,000–$249,000. “Feeling numb or checked out” follows the same pattern: 13% of low earners versus 2% of high earners.

This emotional dimension of savings behavior is often overlooked in financial product conversations, but it matters enormously. People who feel embarrassed about their finances are less likely to engage with financial products, less likely to seek advice, and less likely to take steps — even simple ones — that could improve their situation.

Shame creates avoidance, and avoidance can be expensive. But closing this emotional gap may simply be about better communication and framing.

Research backs this up with specificity. A 2021 study published in Organizational Behavior and Human Decision Processes tracked over 9,000 participants across six studies and found that shame makes people avoid important financial information, creating a vicious cycle that increases hardship. The researchers described it as a “financial shame spiral.”

In short, shame produces avoidance, avoidance produces worse outcomes, and worse outcomes produce more shame. Critically, they found this pattern was unique to shame, not guilt. Guilt can actually motivate repair.

But their data showed that shame tends to encourage retreat instead. For the 15% of lower-income U.S. consumers who describe their savings situation as embarrassing, that cycle is likely already in motion.

This survey reveals a population that’s trying to save under uncertain conditions and making decisions that are, in context, entirely rational.

The preference for liquid savings over locked returns makes sense when one surprise expense could destabilize a household. The reluctance to commit to a fixed-term product makes sense when monthly withdrawals are already a financial norm. The anxiety women carry into savings decisions makes sense in a broader context of gender-based economic inequity that has never fully resolved.

What’s striking is that the appetite for better savings tools is clearly there. More than 89% of U.S. consumers would consider locking up savings if the right safety net came with it. The gap between that intent and action is a gap in trust rather than knowledge.

They don’t trust that the product will work for them when it matters most, that they won’t be penalized for life’s unpredictability, or that they have enough financial stability to take even a small step toward the future.

That kind of trust isn’t built by a product feature alone. But it’s a start.

Find the full survey and responses here.

To understand how U.S. consumers approach saving and financial decision-making, we surveyed 1,000 adults across the country who were familiar with savings products like CD’s. Participants answered a series of questions about their savings habits, emotional relationship with money, and willingness to lock funds away for a guaranteed return versus keeping them accessible. Responses were analyzed by demographic groups including age, gender, and household income to identify trends and disparities.

Readers are welcome to utilize the insights and findings from this study for noncommercial purposes, such as academic research, educational presentations, and personal reference. When referencing or citing this article, please ensure proper attribution to maintain the integrity of the research. Direct linking to this article is permissible, and access to the original source of information is encouraged.

For commercial use or publication purposes, including but not limited to media outlets, websites, and promotional materials, please contact the authors for permission and licensing details. We appreciate your respect for intellectual property rights and adherence to ethical citation practices. Thank you for your interest in our research.

This material is for informational purposes only and is not intended to replace the advice of a qualified tax advisor, attorney or financial advisor. Readers should consult with their own tax advisor, attorney or financial advisor with regard to their personal situations.

Tue Apr 07 2026

A new survey reveals how many U.S. consumers trust AI for financial advice — and why human advisors still hold an edge.

Tue Feb 10 2026

We surveyed 1,000 people to find out how rising costs, lack of savings and income uncertainty may be shaping personal finances in 2026.

Tue Jan 27 2026

A new U.S. consumer survey reveals financial success is evolving — less about status, more about freedom, peace of mind, and control over time.