Tue Feb 10 2026

Groceries, Debt and Doubt: The Financial Mood of U.S. Consumers Heading Into 2026

We surveyed 1,000 people to find out how rising costs, lack of savings and income uncertainty may be shaping personal finances in 2026.

FDIC-Insured - Backed by the full faith and credit of the U.S. Government

April 07, 2026

A new survey reveals how many U.S. consumers trust AI for financial advice — and why human advisors still hold an edge.

In this article:

When financial uncertainty arises, people look for guidance. For decades, that meant a call to a financial advisor or a conversation with someone they trust.

Now, artificial intelligence (AI) is entering that decision-making process.

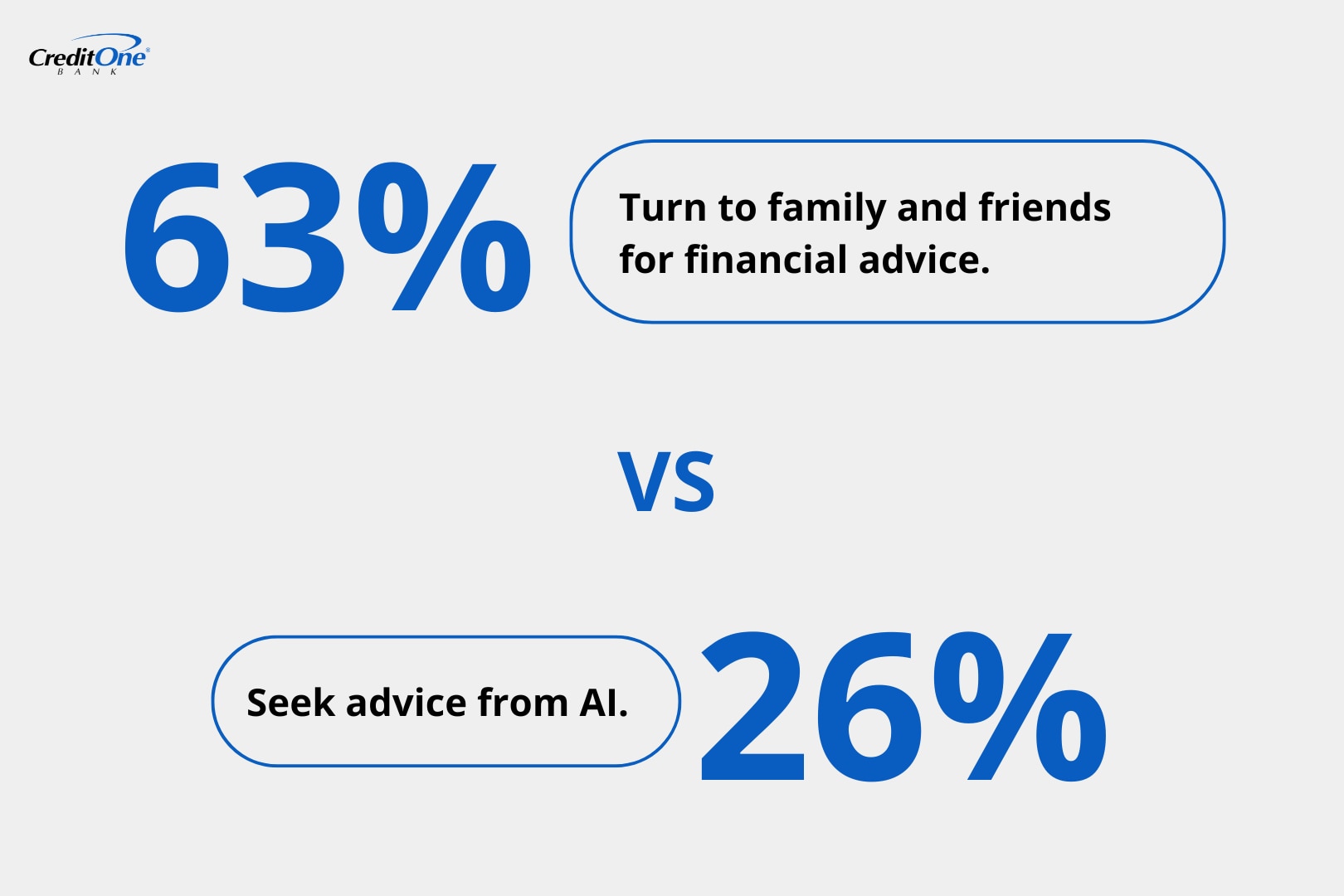

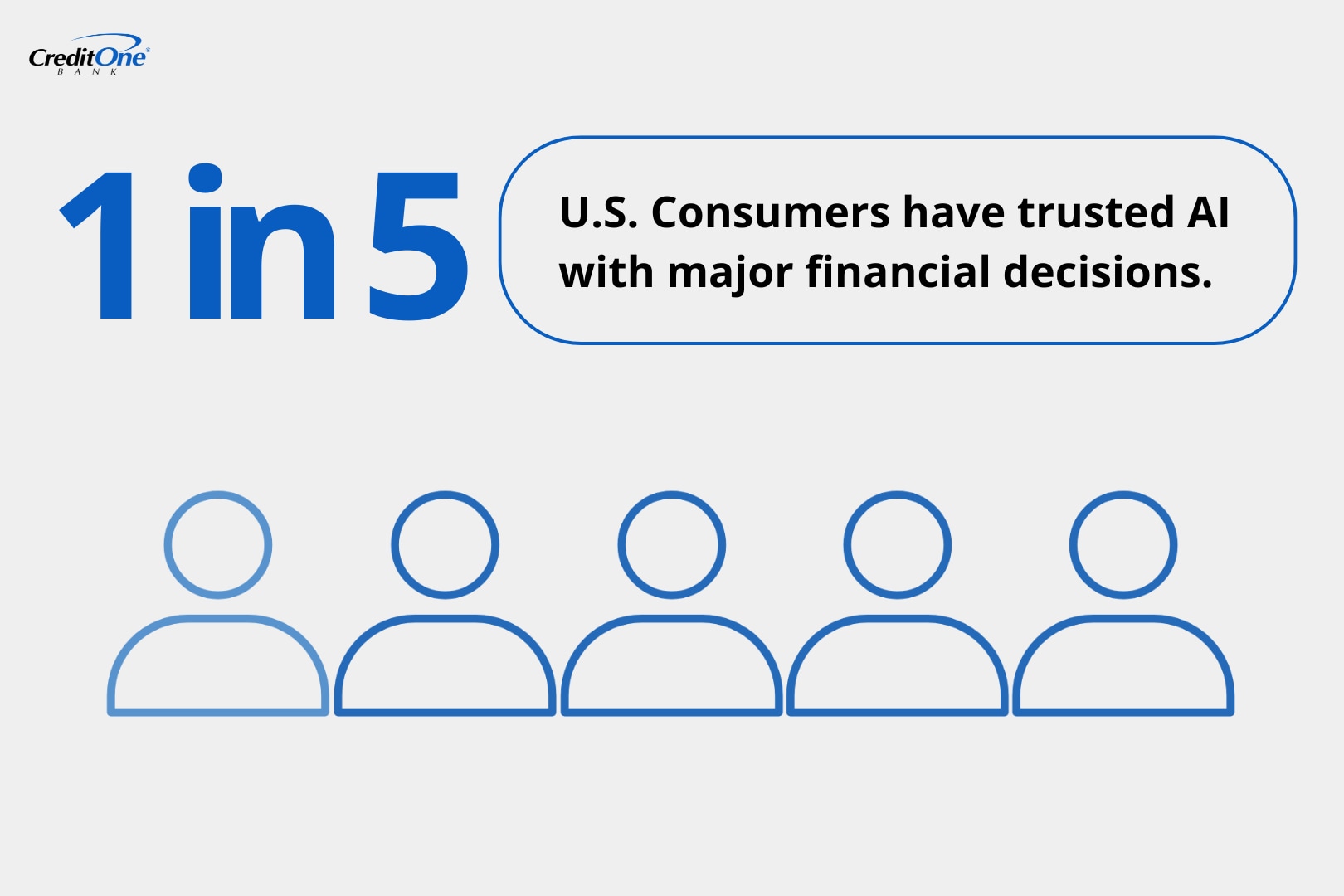

New survey data shows that 26% of U.S. consumers have sought financial advice from an AI-powered app or chatbot in the past year. Even more telling, 20% say they have made a significant financial decision primarily based on an AI tool’s recommendation.

The findings reflect a broader national conversation about artificial intelligence in everyday life. Consumers are experimenting with AI tools for everything from budgeting to investing, yet concerns about privacy and accuracy continue to shape how deeply they engage.

Recent industry moves suggest that AI financial advisors are moving out of theory and into practice. In April 2026, OpenAI acquired Hiro Finance, a startup that helps users model financial decisions and plan their money using AI. While the company has not outlined specific plans for consumer finance, the move could signal a growing interest in expanding AI-powered financial tools and capabilities.

So even though the technology is gaining ground, trust is still being negotiated.

63% sought financial advice from family or friends in the past year

26% used an AI-powered app or chatbot for financial advice

34% of millennials used AI tools for financial advice

20% made a significant financial decision based primarily on AI

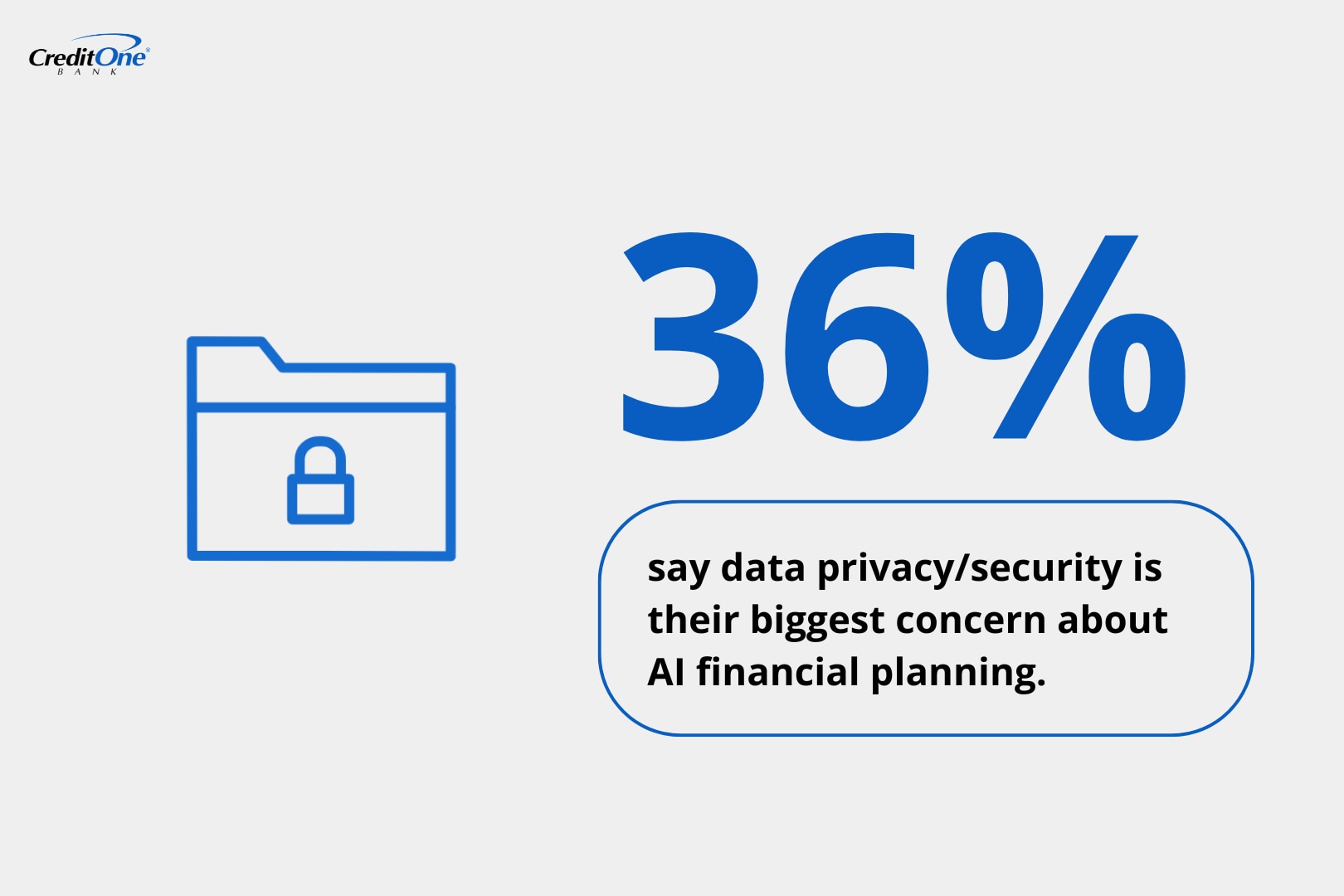

36% of U.S. consumers cite data privacy as their biggest concern about AI financial planning

60% are more likely to trust advice backed by a major financial institution

AI may be expanding into personal finance, but human advice remains dominant.

Nearly 63% of U.S. consumers say they turned to family or friends for financial guidance in the past year. That gap between informal human advice and AI use is significant.

Financial advice is not only about numbers. Money decisions can carry emotional weight. Conversations with people provide reassurance and context in a way that algorithms cannot. That dynamic is reflected in how consumers prioritize different financial needs, from building strong credit habits to bolstering their savings.

The data suggests that while U.S. consumers are open to AI tools, they have not abandoned personal trust networks.

Age plays a clear role in adoption.

Among millennials, 34% have sought financial advice from an AI tool. For many consumers that have grown up using technology for research and decision-making, AI becomes another source of input rather than a radical departure from traditional advice.

Public perception reinforces this generational divide. 65% of U.S. consumers believe Gen Z is the generation most likely to trust AI over human advisors. The expectation itself reflects how strongly AI is associated with younger consumers.

The most striking finding may be how far AI has moved beyond experimentation.

One in five U.S. consumers (20%) reports making a significant financial decision primarily based on AI recommendations. That includes decisions with long-term financial impacts.

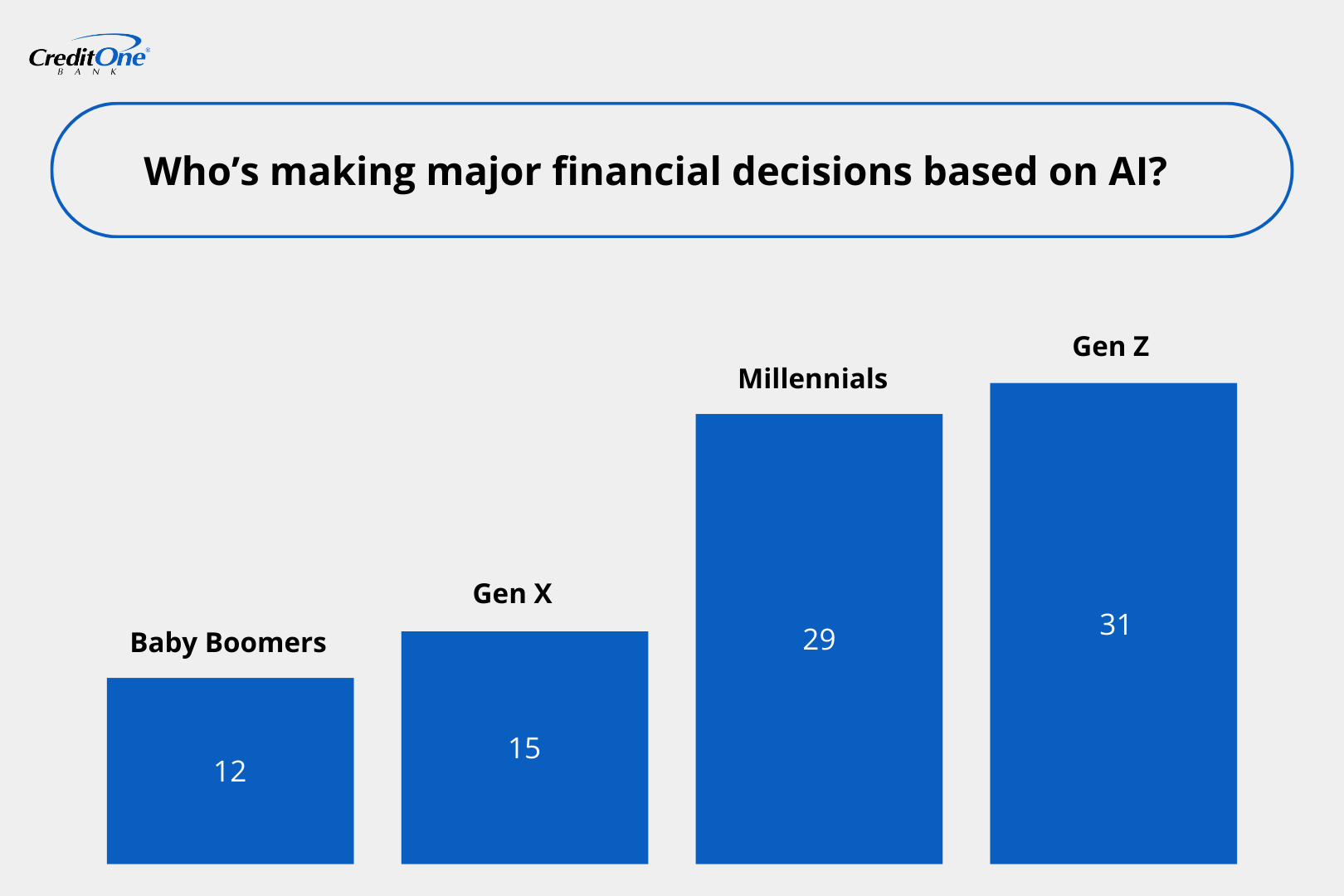

A similar pattern of reliance shows across generations, though the nuances tell a more interesting story. 12% of Baby Boomers have relied on AI compared to 15% of Gen X and 29% of Millennials. Even among the most digitally native generation, less than a third (31%) of Gen Z have relied on AI for major financial decisions, the highest share of any generation, yet still a minority. It suggests that growing up with technology does not automatically translate into trusting it with your financial future.

Despite this, U.S. consumers do not appear to shift responsibility to the technology. Regardless of generation, personal accountability remains a constant: 40% say they would hold themselves accountable if an AI-guided decision resulted in substantial losses. AI may expand access to financial guidance, but consumers still approach recommendations with an emphasis on making informed financial decisions.

The tool may guide, but the individual remains responsible.

Enthusiasm for AI tends to be balanced by caution. The leading concern, cited by 36%, is data privacy and security. Close behind, 33% worry about the accuracy of AI-generated financial advice.

The data suggests that protecting financial information is a priority for many consumers before engaging with digital tools. Sharing income, debt levels, and investment details with an automated system requires confidence in both protection and precision.

Gender differences highlight that caution is not uniform. 41% of men say they would feel comfortable sharing their full financial data with an AI system, compared to 25% of women. Trust levels follow a similar pattern, with 15% of men saying they trust AI more than a human advisor, versus 10% of women.

So it seems that adoption is closely tied to the perceived risk.

Being connected to a known brand or institution appears to reduce uncertainty around AI-powered recommendations. About 60% of U.S. consumers say they’re more likely to trust financial advice if it comes from a source backed by a major financial institution.

Access through employers could accelerate adoption. 54% say they would likely use an AI-powered financial planning tool if offered as a free workplace benefit.

The findings suggest that AI’s growth in financial advising may depend less on replacing institutions and more on operating within them.

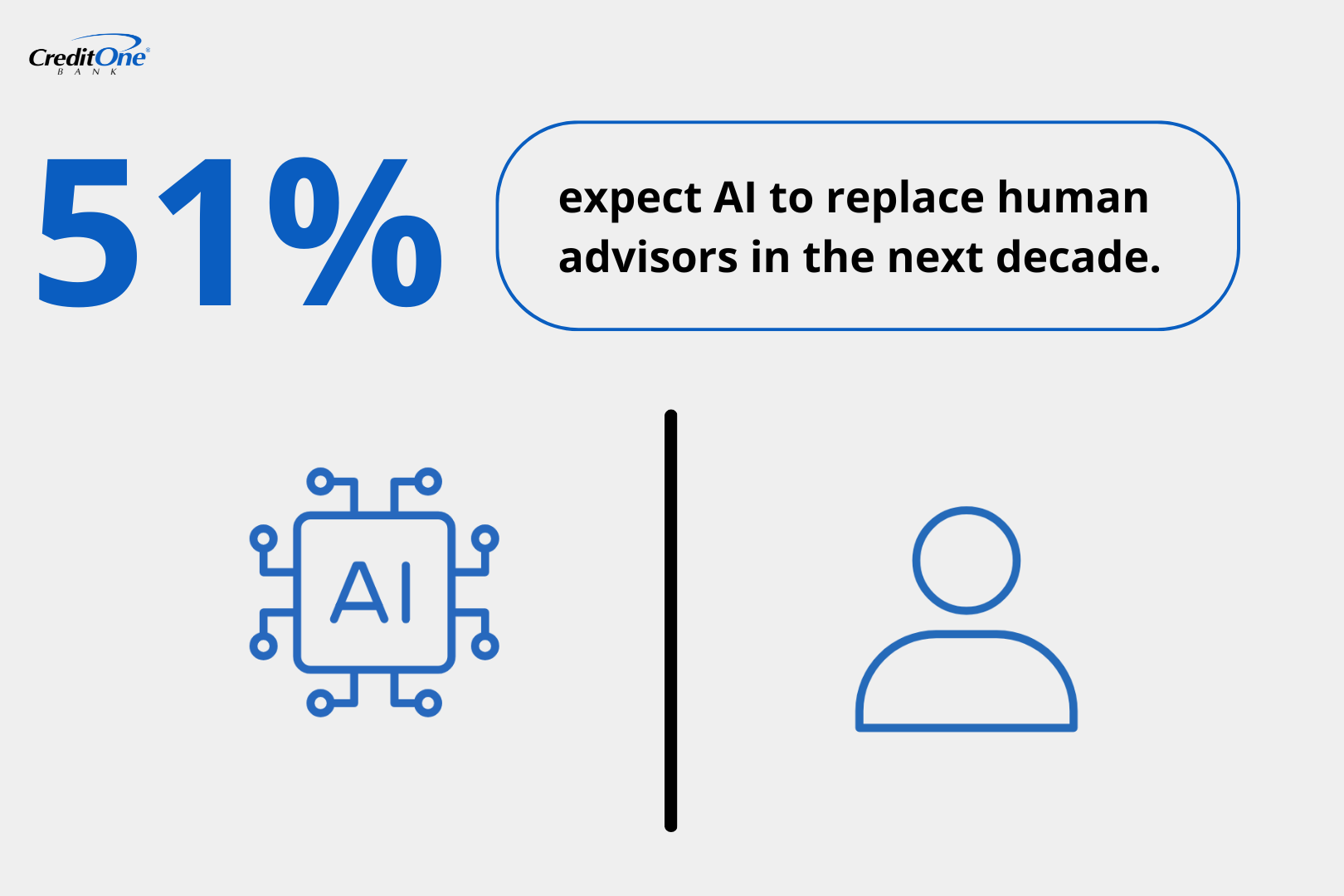

More than half of U.S. consumers (51%) believe AI will replace most financial advisors within the next decade.

Public debate often frames AI as a replacement for professionals across industries. But in financial advising, consumer behavior suggests a more gradual shift, with many U.S. consumers using AI as support rather than a substitute.

Expectations vary by income level. 55% of those earning under $50,000 believe a replacement is likely, compared to 46% of those earning $150,000 or more.

Lower-income respondents may see AI as a more affordable path to financial guidance. Higher-income earners may view human advisors as a tailored service that technology cannot fully replicate, particularly for complex planning or long-term financial strategy decisions.

Yet comfort levels suggest the transition will not be immediate. Only 31% say they would feel comfortable sharing their full financial data with an AI system for personalized advice.

So U.S. consumers may expect change, but they are still weighing how far to go.

AI has moved from a novelty to an influential force in personal finance. Millions of U.S. consumers are already consulting it, and a significant share are acting on its recommendations.

At the same time, trust in humans and known institutions remain dominant, while security concerns persist. If these trends hold, the future of financial advice appears less like a replacement story and more like a recalibration.

Find the full survey and responses here.

To understand how U.S. consumers approach AI-powered financial advice compared with traditional human advisors, we surveyed 1,000 adults nationwide via Pollfish. Participants answered a series of questions about where they seek financial guidance, their level of trust in AI tools compared to human advisors, whether they have made major financial decisions based on AI recommendations, and their concerns around privacy, accuracy, and data security.

Responses were analyzed by age, income, gender, and ethnicity to identify generational trends, differences in trust, and disparities in adoption across demographic groups.

Readers are welcome to utilize the insights and findings from this study for noncommercial purposes, such as academic research, educational presentations, and personal reference. When referencing or citing this article, please ensure proper attribution to maintain the integrity of the research. Direct linking to this article is permissible, and access to the original source of information is encouraged.

For commercial use or publication purposes, including but not limited to media outlets, websites, and promotional materials, please contact the authors for permission and licensing details. We appreciate your respect for intellectual property rights and adherence to ethical citation practices.

This material is for informational purposes only and is not intended to replace the advice of a qualified tax advisor, attorney or financial advisor. Readers should consult with their own tax advisor, attorney or financial advisor with regard to their personal situations.

Tue Feb 10 2026

We surveyed 1,000 people to find out how rising costs, lack of savings and income uncertainty may be shaping personal finances in 2026.

Mon Dec 08 2025

Many people think they know a lot about credit. But as it turns out, there may be some crucial knowledge gaps among consumers.

Mon Oct 20 2025

What’s in a number? Find out how adults from two distinct generations factor in credit scores and financial habits as they assess relationships.