Fri Oct 17 2025

Study Reveals One Third of Credit Card Users Hide Debt from Loved Ones and Family

Opening your first credit card? We surveyed first-time credit card users. Find out about their experience with debt, financial literacy and more.

FDIC-Insured - Backed by the full faith and credit of the U.S. Government

December 08, 2025

Many people think they know a lot about credit. But as it turns out, there may be some crucial knowledge gaps among consumers.

In this article:

Your credit score is one of the most important numbers in your financial life, yet it remains a mystery to many. To find out what people really know about their credit, we conducted a new survey with 1,000 U.S. consumers. We asked them about everything from where they learned about credit to how scores are calculated. And what we found was a lot of confusion and costly misconceptions.

From believing common myths about closing old cards to misunderstanding how rent and minimum payments affect their scores, we uncovered the most significant gaps in financial knowledge that could be holding people back from achieving their financial goals.

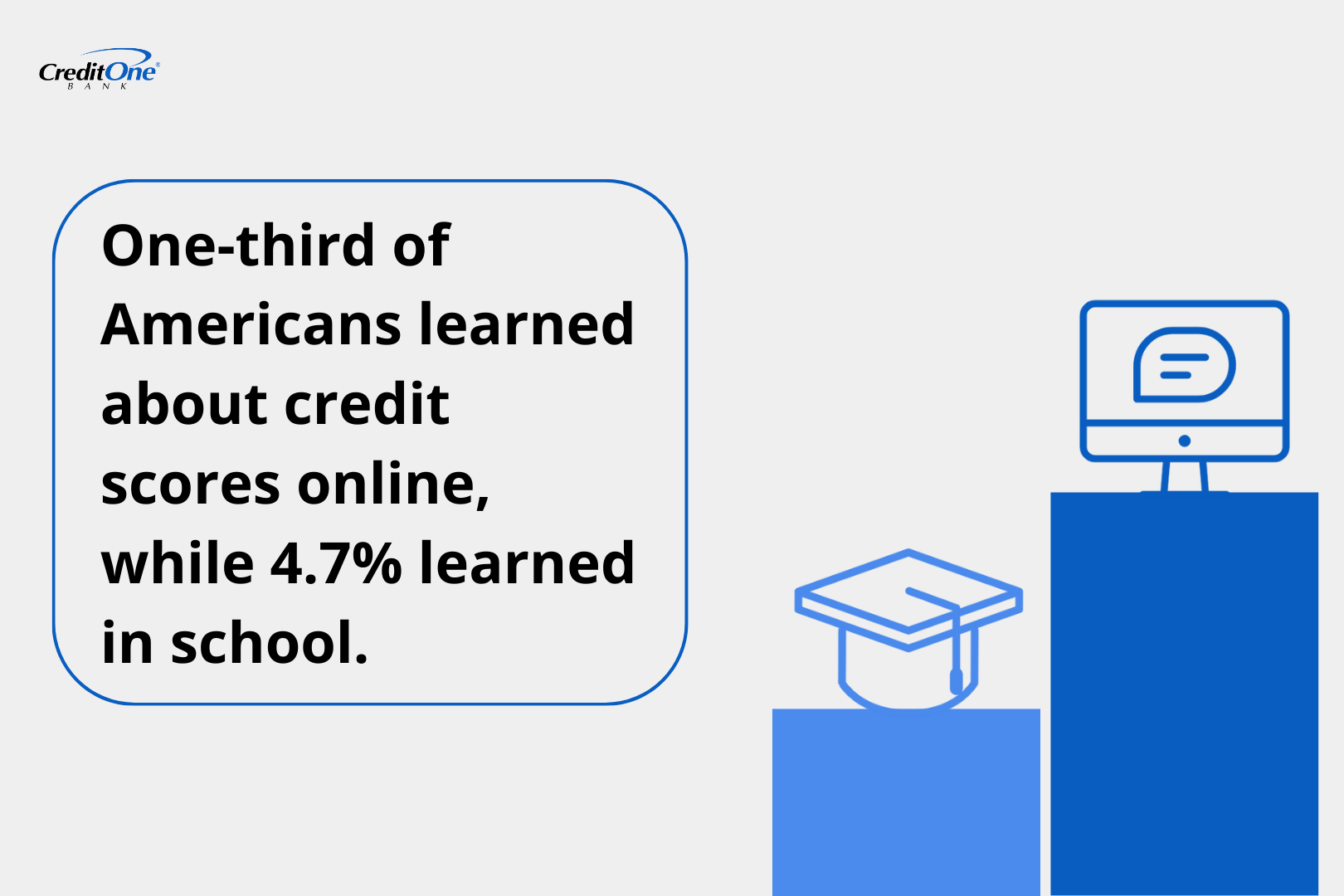

33% of U.S. consumers have learned the most about how credit scores work from online sources. Less than 5% report that they learned the most about how credit scores work from school or university courses.

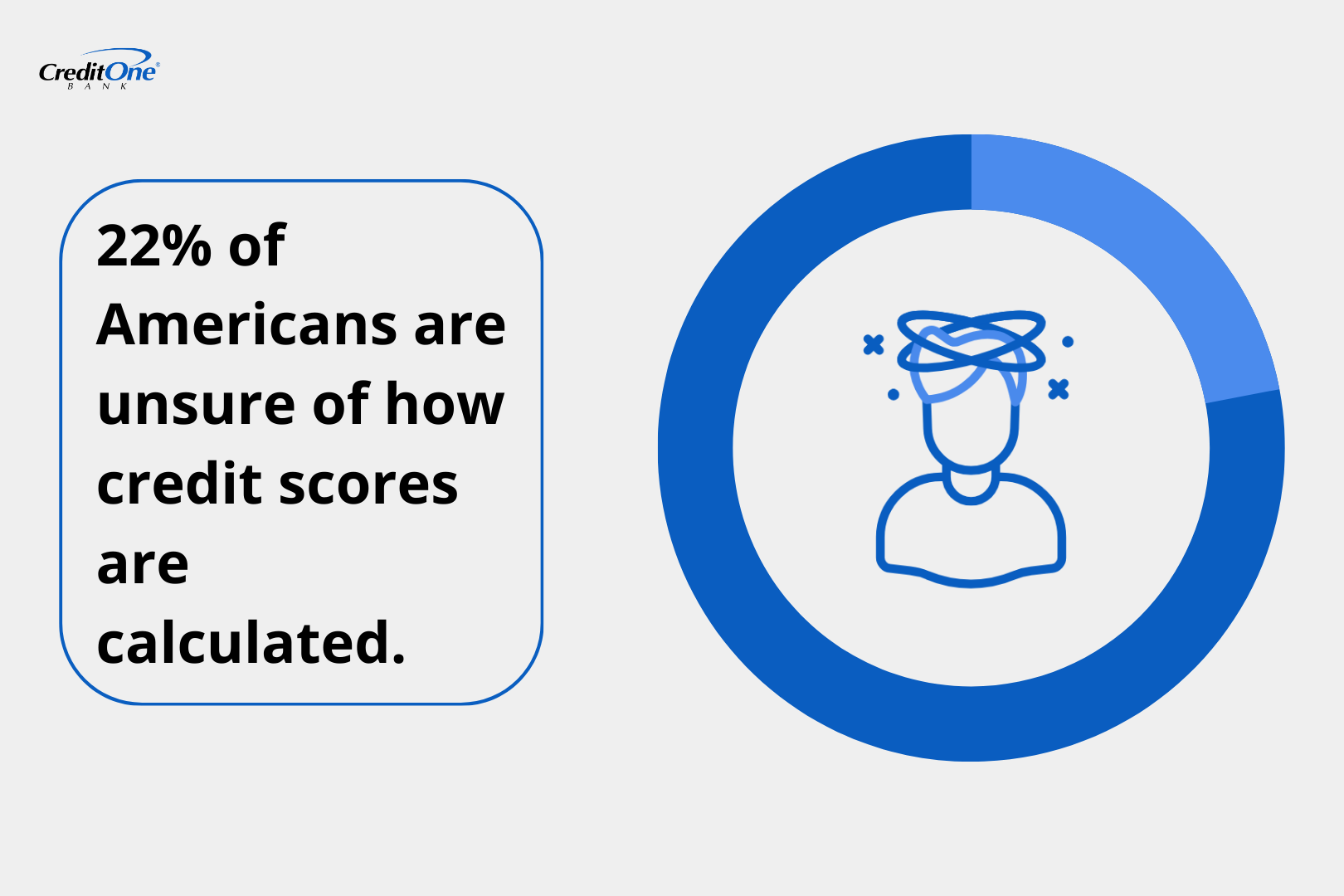

22% are not confident in their understanding of how credit scores are calculated.

35% regularly use an app or tool to track their credit score, and 14% of Gen Zers admit to never checking their credit score.

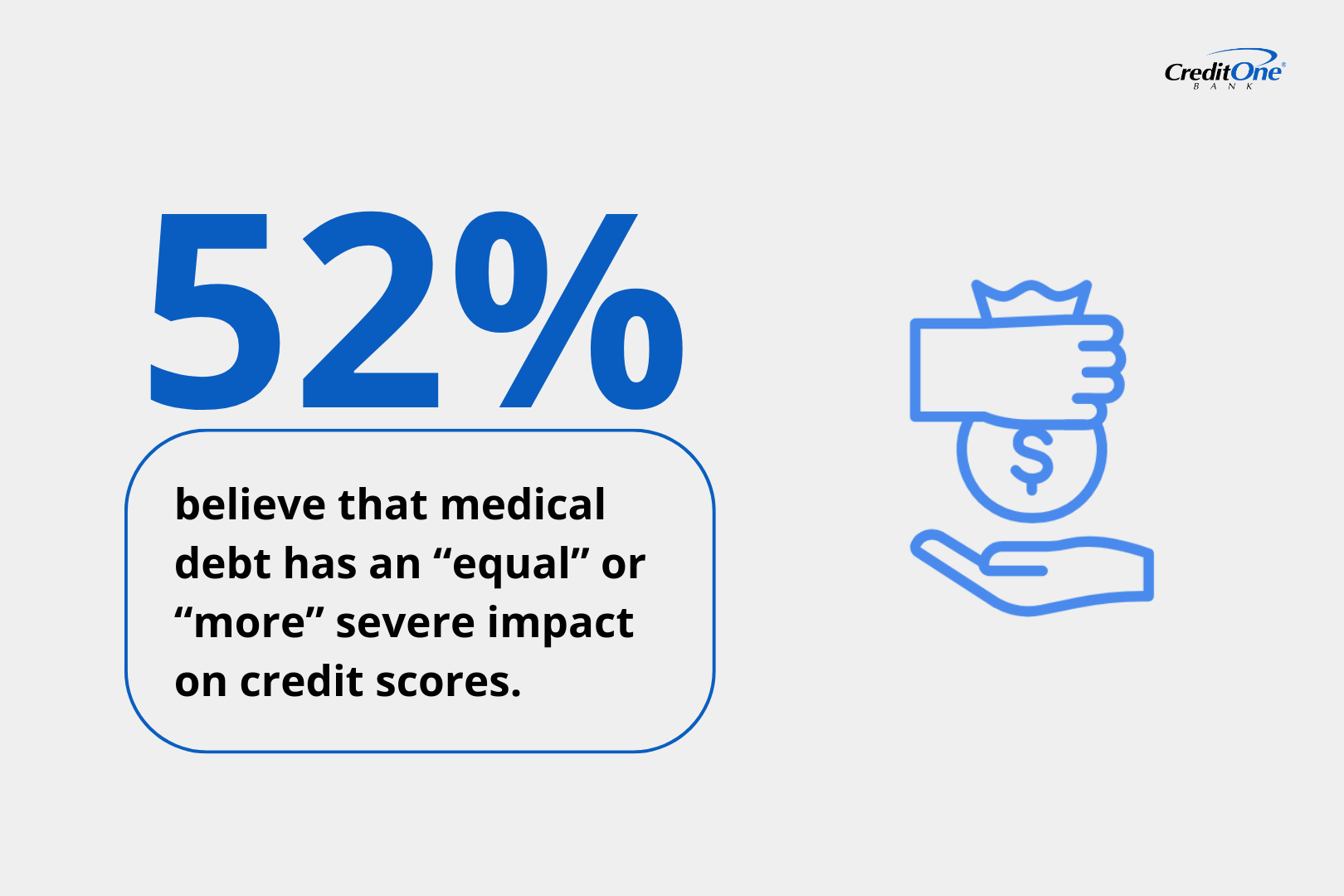

52% believe medical debt has an “equal” or “more severe” impact on credit scores than other types of debt.

53% of Americans do not know that closing an old credit card is likely to hurt their credit score.

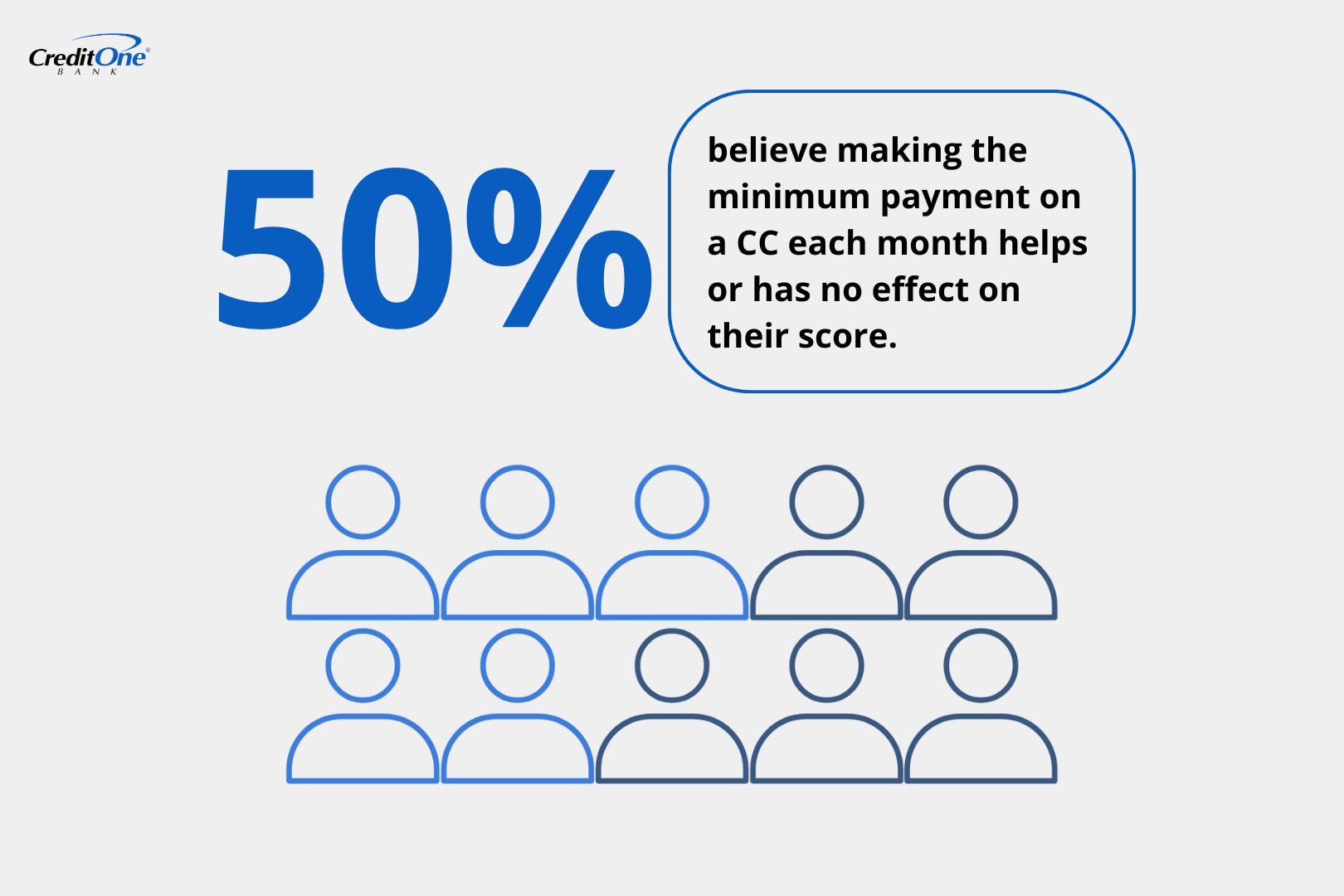

50% believe that making only the minimum payment on a credit card each month helps or has no effect on their score.

39% believe paying rent on time is automatically included in credit score calculations.

When it comes to understanding credit scores, U.S. consumers are far more likely to learn about credit from the internet than from formal education.

33% of U.S. consumers have learned the most about how credit scores work from online sources, while only 4.7% learned through school or university courses.

This sevenfold gap highlights the absence of credit education in traditional curricula, leaving most U.S. consumers to piece together their financial literacy online. Without structured guidance, misinformation can easily spread, and small misunderstandings can have lasting financial consequences.

This reliance on self-guided, online learning may explain another key finding from our recent study. Even with widespread online resources, many still feel unsure about how credit scores are calculated.

22% of U.S. consumers say they’re not confident in their understanding of how credit scores are calculated.

This lack of confidence points to a deeper issue: access to information doesn’t always equal understanding. Many people may know where to find credit advice but struggle to determine what’s accurate, which can lead to costly mistakes in managing their financial health.

Technology has made it easier than ever to stay on top of your financial profile, but not everyone is taking advantage of it.

35% of U.S. consumers regularly use an app or digital tool to track their credit score.

Meanwhile, 14% of Gen Z over the age of 18 admit they never check their score at all.

This generational divide highlights a paradox: even in the most tech-savvy generation, a significant portion remains disconnected from their credit health, potentially missing opportunities to establish strong financial foundations early.

This disconnect in financial habits is often rooted in deep-seated anxieties about specific types of debt. Medical debt remains a major source of anxiety for many households, but perceptions haven’t caught up with reality.

52% of U.S. consumers believe medical debt has an equal or greater impact on their credit score than credit card or personal loan debt.

In truth, recent changes by major credit bureaus have minimized the effect of medical debt under $500 on credit reports and lowered the weight of unpaid medical collections in credit scoring models. In addition, 15 states now prohibit the use of medical debt in credit reporting. As a result, millions could have a misplaced concern for their credit health due to medical debt.

This confusion isn’t limited to complex issues like medical debt — it also extends to some of the most basic principles of credit management. Many people think closing old credit cards is a responsible move, but it often backfires.

53% of Americans do not know that closing an old credit card is likely to hurt their credit score.

Closing an account, particularly a long-held one, can negatively impact two critical components of a credit score: the length of your credit history, including the average age of open accounts, and your credit utilization ratio.

In reality, this can lower your score by reducing your total available credit and shortening your credit history under some credit scoring models. This “financial decluttering” habit can actually cause more harm than good, illustrating how small misconceptions can have large financial repercussions.

Perhaps the most financially damaging misconception we uncovered relates to the routine act of paying the monthly credit card bill. Paying the minimum each month may seem like a safe move, but it’s a costly mistake.

50% of U.S. consumers believe that making only the minimum payment either helps or doesn’t affect their score.

While this approach avoids late fees and contributes to establishing a positive payment history, it can keep balances high and increase your credit utilization ratio, a key factor that can drag down your score. This misconception keeps many consumers in a cycle of debt and damaged credit.

A massive source of confusion we found centers on one of the largest monthly expenses for many people: rent. For millions of renters, paying on time every month doesn’t necessarily translate into an improvement in their credit.

39% of U.S. consumers believe rent payments are automatically factored into their credit score.

In most cases, landlords don’t report rent payments to credit bureaus (Equifax, Experian, and TransUnion), meaning responsible tenants often receive no credit for their consistent payments. This lack of reporting creates a blind spot in credit systems, making it more difficult for renters to demonstrate their financial reliability.

While a history of non-payment can eventually end up on your credit report if you’re evicted or sent to collections, the positive history of consistent, on-time payments may go unrecorded — unless you use a rent-reporting service or an app like Experian Boost, which can incorporate rent and utility payments.

While our study highlights that the world of credit is filled with myths and confusion, the takeaway isn’t one of fear — it’s one of empowerment. Every misconception you’ve read about here is now a piece of knowledge you can use to your advantage.

Your credit score isn’t a permanent grade written in stone. Think of it instead as a living number that you have the power to shape and grow. By understanding the real rules of the game, you can move forward with confidence, making smart, informed decisions that build a stronger and brighter financial future, one step at a time.

Find the full survey and responses here.

To understand how U.S. consumers approach credit education and credit score management, we surveyed 1,000 adults across the United States in November 2025 using the Pollfish online survey platform. Participants answered a series of questions about where they learned about credit, how confident they feel in understanding how credit scores are calculated, and common beliefs about factors that influence credit health.

Responses were analyzed across age, gender, and generation to identify knowledge gaps, behavioral trends, and misconceptions surrounding credit education and financial literacy.

Readers are welcome to utilize the insights and findings from this study for noncommercial purposes, such as academic research, educational presentations, and personal reference. When referencing or citing this article, please ensure proper attribution to maintain the integrity of the research. Direct linking to this article is permissible, and access to the original source of information is encouraged.

For commercial use or publication purposes, including but not limited to media outlets, websites, and promotional materials, please contact the authors for permission and licensing details. We appreciate your respect for intellectual property rights and adherence to ethical citation practices. Thank you for your interest in our research.

This material is for informational purposes only and is not intended to replace the advice of a qualified tax advisor, attorney or financial advisor. Readers should consult with their own tax advisor, attorney or financial advisor with regard to their personal situations.

Fri Oct 17 2025

Opening your first credit card? We surveyed first-time credit card users. Find out about their experience with debt, financial literacy and more.

Mon Oct 20 2025

What’s in a number? Find out how adults from two distinct generations factor in credit scores and financial habits as they assess relationships.

Wed Oct 22 2025

Current economic uncertainty is causing many consumers to reassess their financial safety nets. Are they relying on emergency savings, turning to credit, or going without?