Mon Oct 20 2025

The Social Status of Credit: How Millennials & Gen Z View Credit Scores

What’s in a number? Find out how adults from two distinct generations factor in credit scores and financial habits as they assess relationships.

FDIC-Insured - Backed by the full faith and credit of the U.S. Government

October 17, 2025

Opening your first credit card? We surveyed first-time credit card users. Find out about their experience with debt, financial literacy and more.

In this article:

Credit One Bank surveyed 1,000 first-time credit card users and uncovered how young adults are stepping into the world of credit with a sense of optimism, while also facing challenges.

The data highlights concerning trends such as secrecy, confusion, and facing early consequences that can impact credit history. It also underscores the opportunity to strengthen financial education and empower strategic credit use for the future.

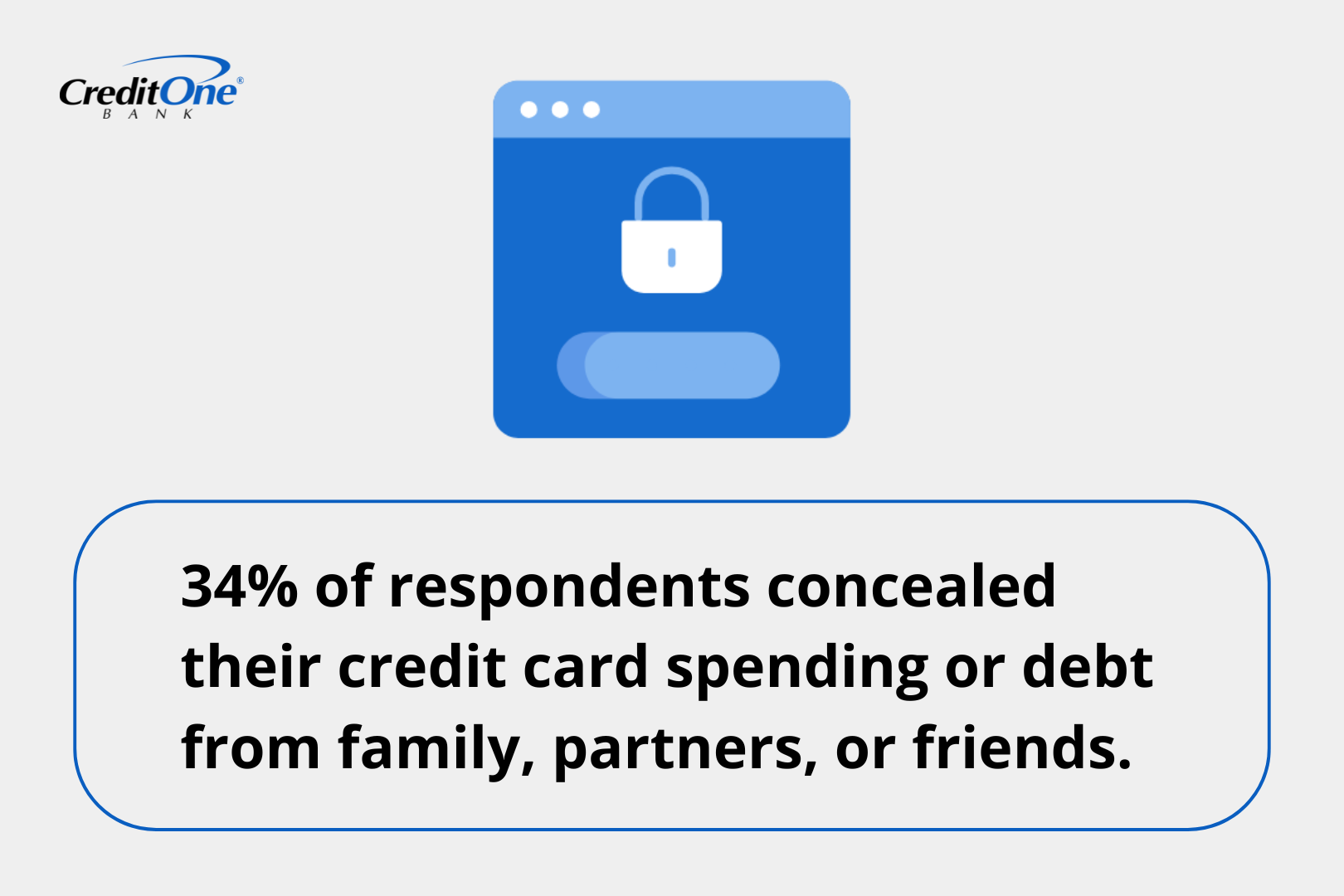

Financial secrecy is surprisingly common among new cardholders, with 34% of first-time cardholders admitting to hiding debt or spending from family, partners, or friends.

Avoiding open conversations about money can leave young adults struggling on their own.

This secrecy often stems from feelings of shame or fear of judgment. Instead of seeking support, many bury their struggles, which can lead to missed payments, deeper debt, and damaged credit scores. Open dialogue with family and friends could help cardholders find advice earlier and avoid these costly mistakes.

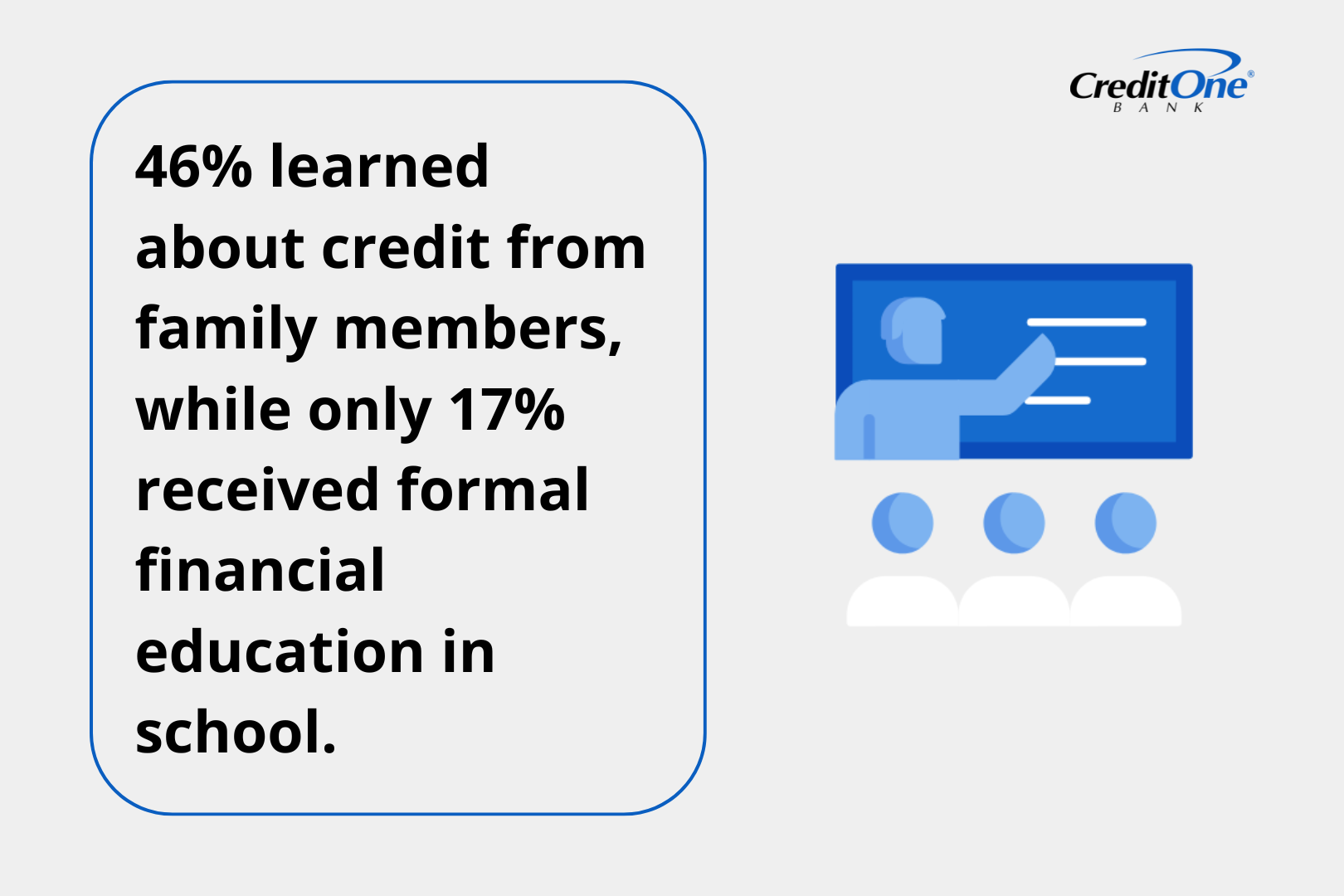

The survey shows family conversations, rather than textbooks, are likely to introduce people to credit.

Among respondents, 46% learned about credit from family members and only 17% received formal financial education in school.

While this can provide a sense of trust and relatability, it also means that financial lessons are passed down unevenly and sometimes inaccurately.

When financial knowledge is inherited rather than formally taught, young adults may unknowingly absorb poor habits right alongside good ones. In fact, past research has shown how these patterns can create generational financial trauma — where debt cycles, risky credit behaviors, or money avoidance are repeated from one generation to the next. Without reliable resources to break that cycle, many first-time cardholders are left with gaps that could limit their financial opportunities.

Families remain an essential first step in shaping financial awareness, but formal credit education can serve as a stabilizing force. By combining trusted family conversations with structured, standardized learning, young adults would be better prepared to manage debt, understand interest, and build credit responsibly. This balance of informal and formal education is key to creating stronger financial foundations for the future.

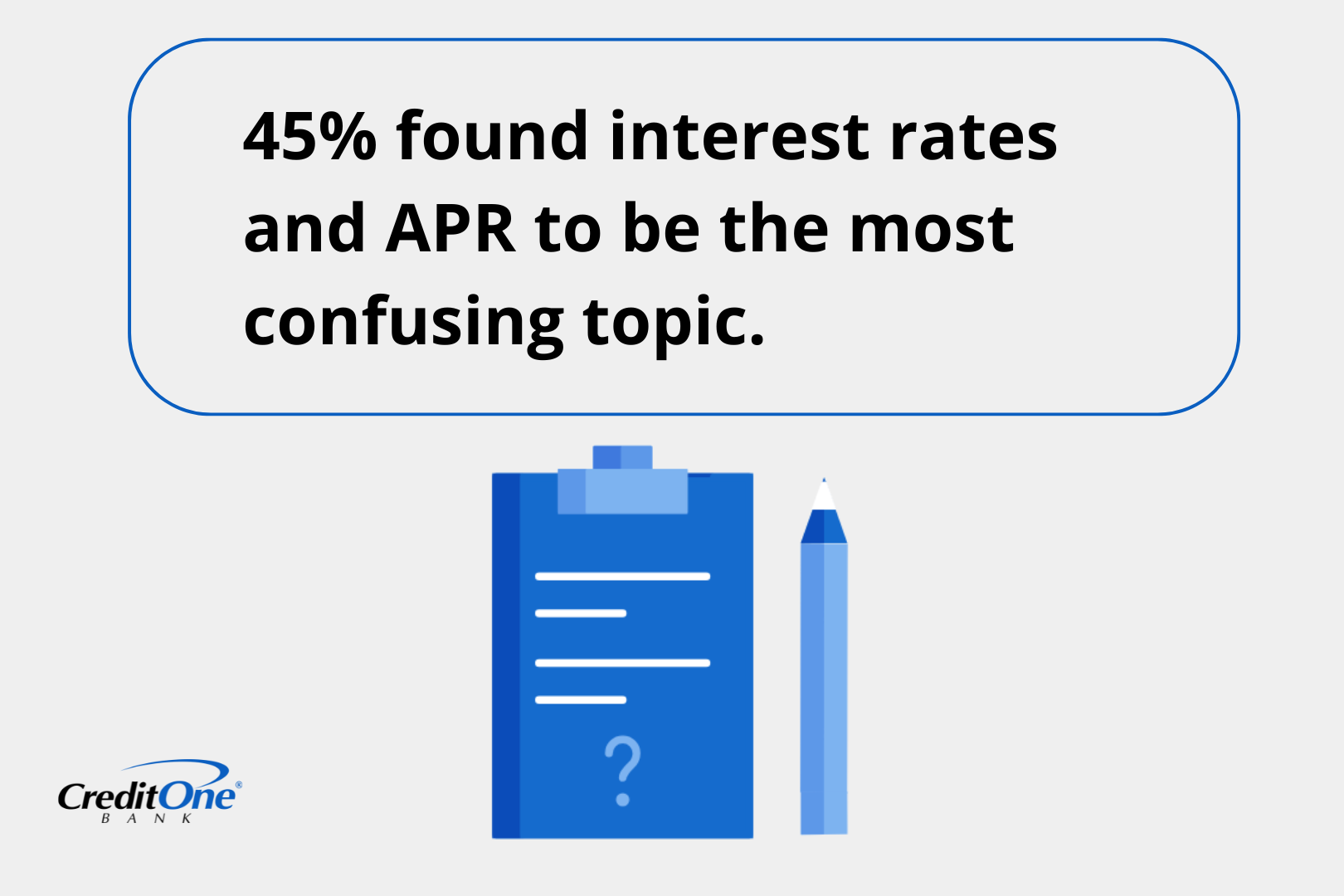

Interest rates are one of the most important aspects of credit cards, yet they remain one of the least understood. Many first-time cardholders know interest exists, but not how it actually compounds or how quickly costs can build up.

A staggering 45% of respondents said that interest rates and APR were the most confusing part of credit cards.

This lack of understanding is more than a minor detail — it directly impacts how expensive borrowing becomes. A balance of just a few hundred dollars can double or triple in size over time if a cardholder only makes minimum payments and doesn’t grasp how interest accrues.

For young adults who are just beginning to build financial independence, this confusion can lead to years of revolving debt, late fees, and damaged credit scores.

The ability to confidently understand APR and interest rates is a turning point for new credit users. With clearer education and better resources, cardholders can avoid the debt spiral and instead use credit cards strategically to build their financial future. Understanding this single concept can often make the difference between a card being a tool for opportunity or a source of long-term stress.

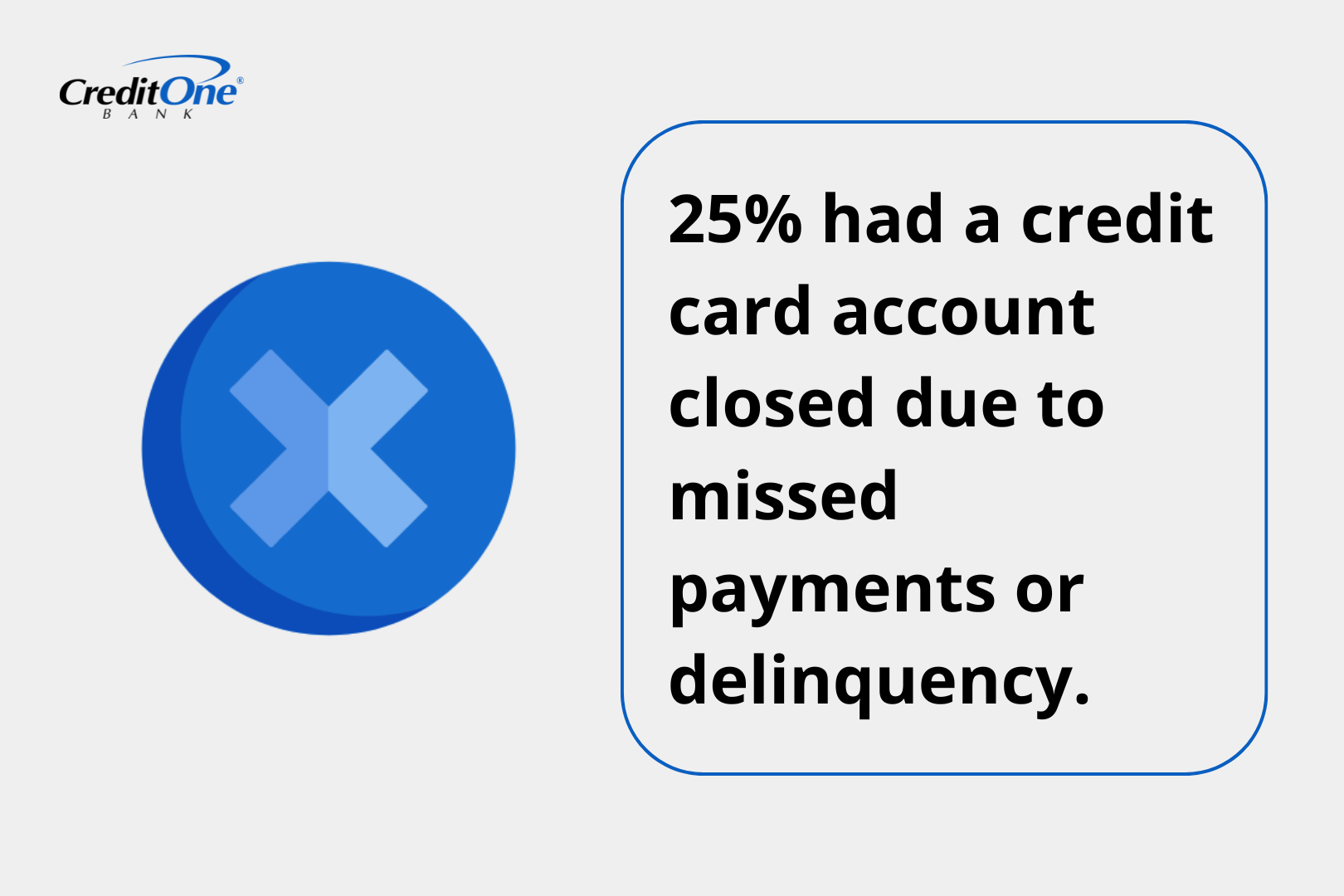

For some, their very first experiences with credit come with serious setbacks.

These closures stay on credit reports for years, potentially limiting access to loans, mortgages, or rentals during key life stages. The data highlights how important education is in helping new cardholders avoid missteps. With proper guidance, early mistakes can be prevented or overcome so credit becomes a useful tool rather than restriction.

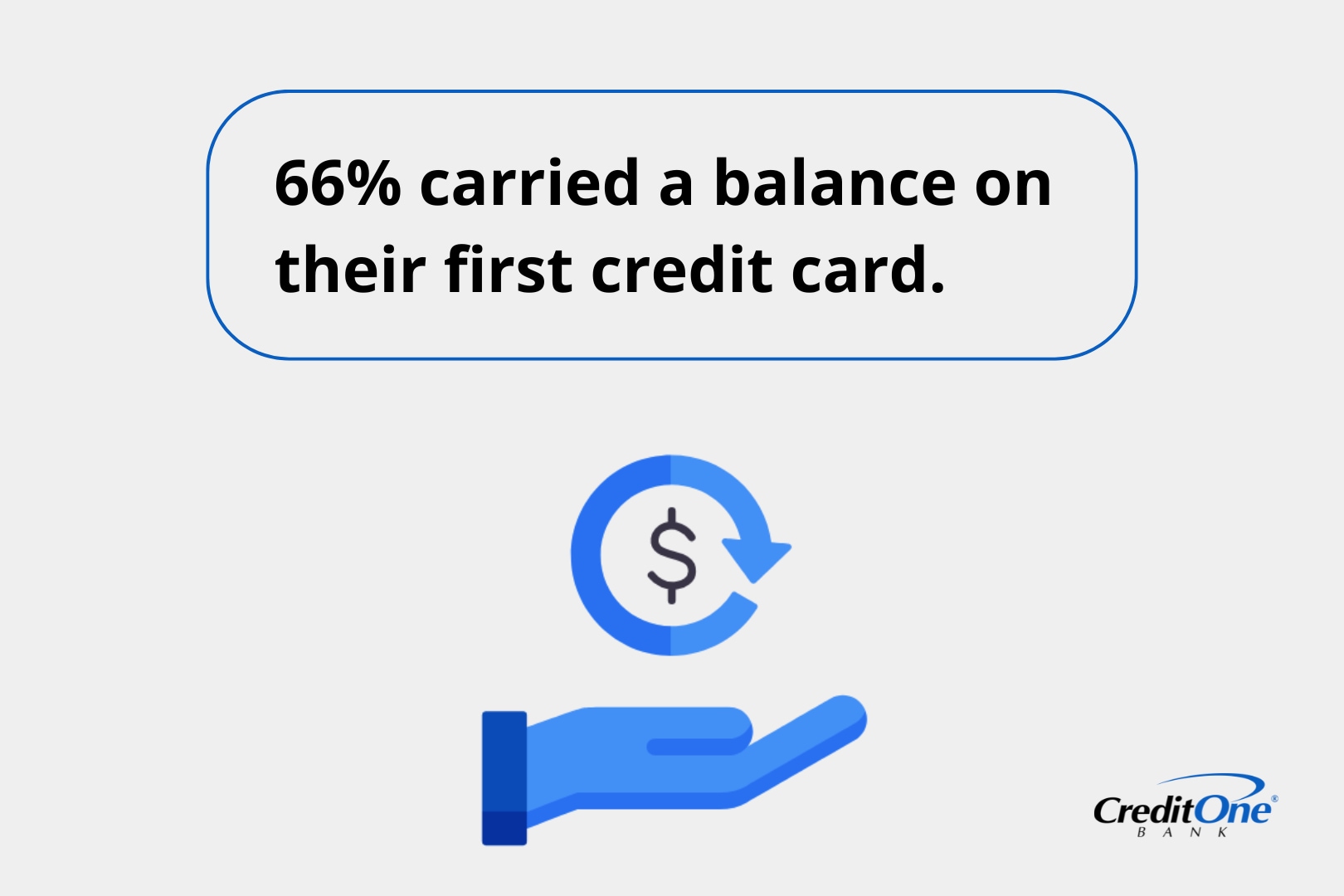

Debt has become the default starting point for many young adults using credit for the first time.

66% of first-time cardholders carried a balance on their first credit card.

Carrying debt so early can feel normal, but it creates long-term risks if left unmanaged. Many young adults start out believing balances are a natural part of credit, when in reality, consistent repayment is the foundation of financial strength. Interest charges can quickly turn small balances into persistent debt. And that debt’s impact on finances and credit history can limit future opportunities like buying a car, qualifying for a loan, or even renting an apartment.

The good news is that adopting healthy credit habits and using debt reduction strategies, especially early on, can help change the trajectory. Teaching cardholders to pay more than the minimum, to understand how interest compounds, and to view credit cards as tools for building rather than borrowing can shift outcomes dramatically. By reframing credit as a resource for growth instead of debt, young adults can turn their first experiences into stepping stones toward financial independence.

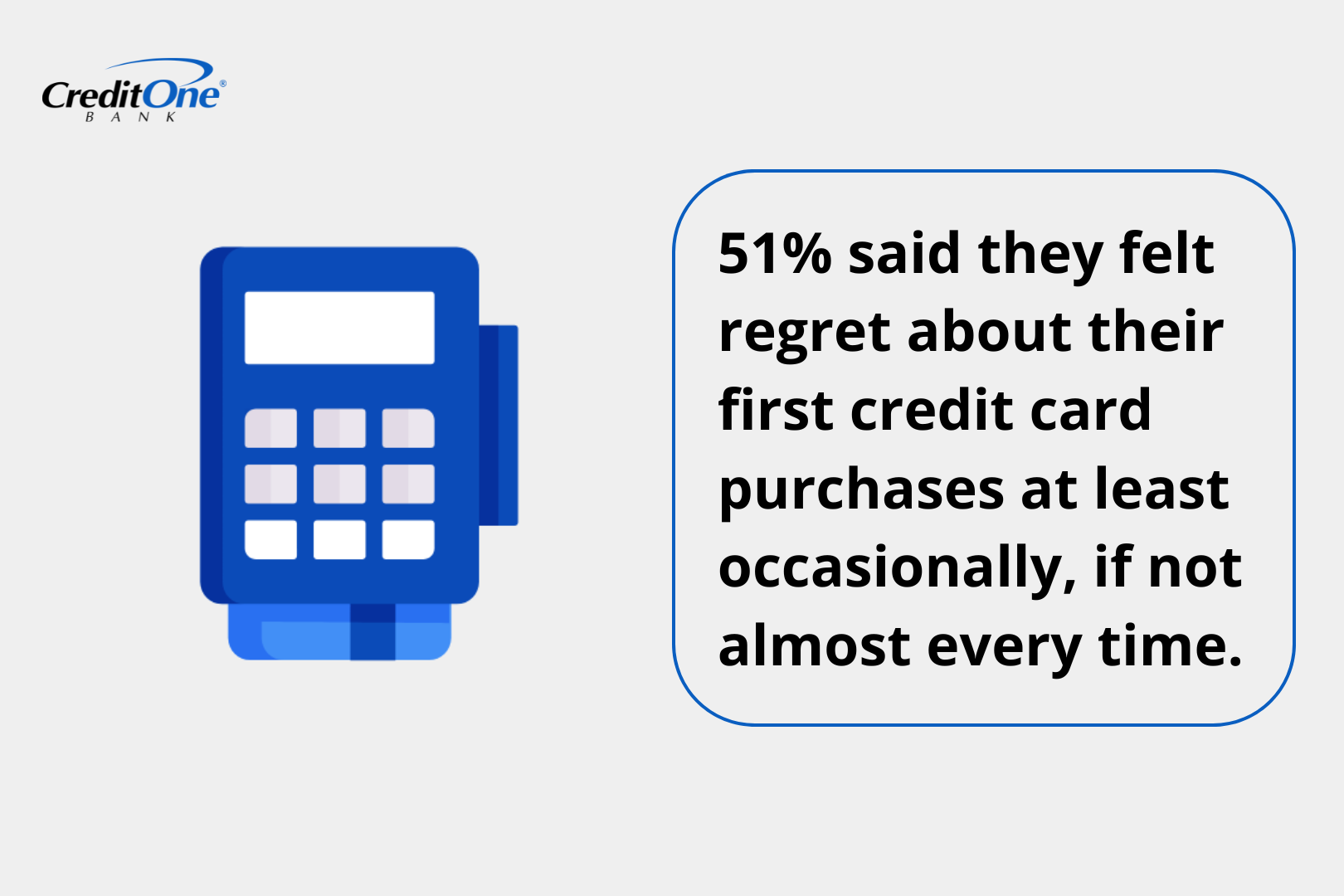

Emotional consequences are just as real as financial ones. Credit cards often make it easier to spend now and worry later, but for many regret quickly follows.

51% of respondents said they felt regret about their first credit card purchases at least occasionally, if not almost every time.

This regret highlights how easily early financial behaviors can become emotional burdens. With education and support, however, those initial regrets can turn into lessons that guide better financial habits moving forward.

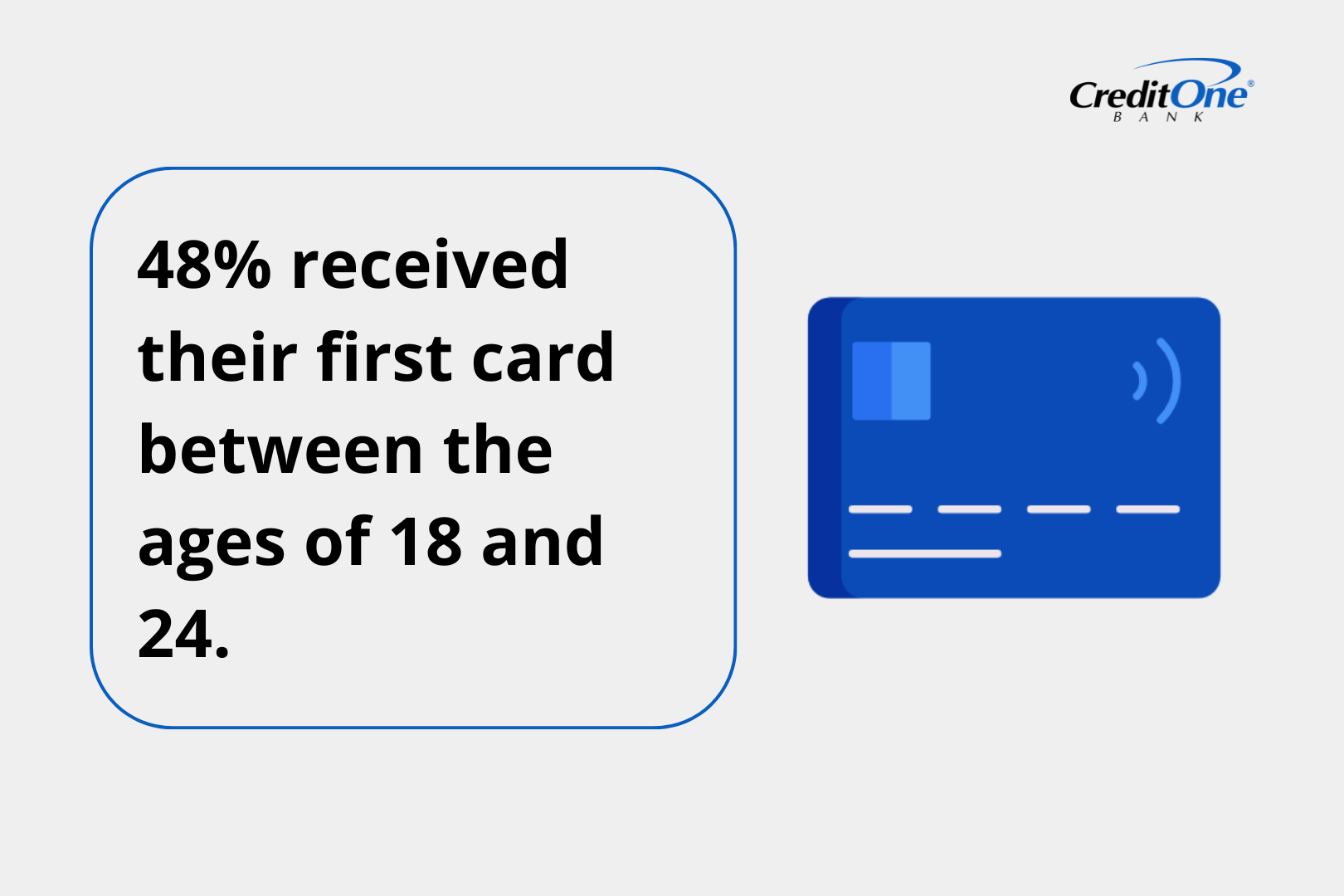

Many cardholders take on credit at a time of major life transitions, with 48% of respondents sharing that they got their first credit card between the ages of 18 and 24.

At this stage in life, they may be off to college, starting in the workplace full time, or living on their own for the first time while also juggling other major life responsibilities. With so much going on, financial literacy may not get the attention it needs.

This timing means critical credit decisions are often made while people are still learning how to manage rent, student loans, and career choices. Without guidance, small mistakes during this period can follow young adults for years, influencing everything from interest rates on future loans to the ability to qualify for housing.

By weaving credit education into this pivotal life stage, financial institutions and educators can help ensure that early experiences with credit lead to healthier habits and stronger opportunities down the road.

The survey findings reveal that while young adults are eager to embrace credit, many enter the system without adequate preparation, leading to secrecy, confusion, and financial missteps.

But that reinforces how important it is to have some early knowledge of credit and debt fundamentals. Many of the financial challenges and emotional consequences revealed by this data can be offset with stronger financial education to promote responsible credit use.

Credit cards aren’t just financial products; they can be powerful tools for building a future. This is why Credit One Bank’s For What’s Ahead initiative exists — to provide people with the knowledge, tools, and confidence they need to use credit strategically.

Find the full survey and responses here.

Credit One Bank surveyed 1,000 first-time credit card users through an online questionnaire, examining early credit experiences and financial literacy.

Participants provided data on their age when obtaining their first card, sources of credit education, understanding of key concepts like interest rates and APR, spending behaviors, debt accumulation, and negative outcomes such as account closures or concealed debt. The survey captured both quantitative spending patterns and qualitative emotional responses to provide insights into how Americans navigate their introduction to consumer credit.

Readers are welcome to utilize the insights and findings from this study for noncommercial purposes, such as academic research, educational presentations, and personal reference. When referencing or citing this article, please ensure proper attribution to maintain the integrity of the research. Direct linking to this article is permissible, and access to the original source of information is encouraged.

For commercial use or publication purposes, including but not limited to media outlets, websites, and promotional materials, please contact the authors for permission and licensing details. We appreciate your respect for intellectual property rights and adherence to ethical citation practices.

This material is for informational purposes only and is not intended to replace the advice of a qualified tax advisor, attorney or financial advisor. Readers should consult with their own tax advisor, attorney or financial advisor with regard to their personal situations.

Mon Oct 20 2025

What’s in a number? Find out how adults from two distinct generations factor in credit scores and financial habits as they assess relationships.

Mon Feb 10 2025

The financial experiences people have early on, whether positive or negative, shape their relationships with money for life. They can affect how people handle paycheck

Wed Oct 22 2025

Current economic uncertainty is causing many consumers to reassess their financial safety nets. Are they relying on emergency savings, turning to credit, or going without?