Thu Feb 04 2021

Loan vs. Line of Credit: What’s the Difference?

If you need to borrow money from a lender (financial institutions like banks or credit unions, not your friends or family), you have two main choices: you can take out a loan or get a

FDIC-Insured - Backed by the full faith and credit of the U.S. Government

Author: Heather Vale

September 16, 2025

It’s important to check your credit report, but even more crucial to understand it. Here’s how to read it and deal with what you see.

If you’ve ever applied for a loan or line of credit, you probably know that your credit score — which is calculated using information contained in your credit reports — is one of the main factors used to make lending decisions. Understanding what your credit reports say about your borrowing and repayment history can help predict how likely you are to be approved for credit, and which rates and terms you may qualify for.

Your credit report is a detailed document that lays out your credit history, including credit inquiries, borrowing history, and public records related to finances. It includes a list of your credit accounts, complete with balances and payment activity.

You have three credit reports because each of the main credit bureaus — Experian, Equifax and TransUnion — generate their own reports based on information they’ve received from lenders. And not every lender or creditor reports the same things to each bureau.

Knowing what’s in your credit report reduces the chances of getting a nasty surprise when you apply for credit. Under the Fair Credit Reporting Act, you’re entitled to receive a free copy of your credit report from each of the three major credit reporting agencies every year. But now you can get free access every week at AnnualCreditReport.com, which is endorsed by the federal government.

A credit report is usually several pages long, but you can take it one piece at a time. Read through each of the sections carefully and thoroughly, then cross-reference them to your records.

Your goal here involves four parts:

Checking your credit report gives you a better idea of how lenders perceive your creditworthiness and what the response will be if you apply for more credit. Most of the information should form a valid representation of your credit history, and this lets you know any habits you need to adopt — like paying on time, every time, and not maxing out your cards.

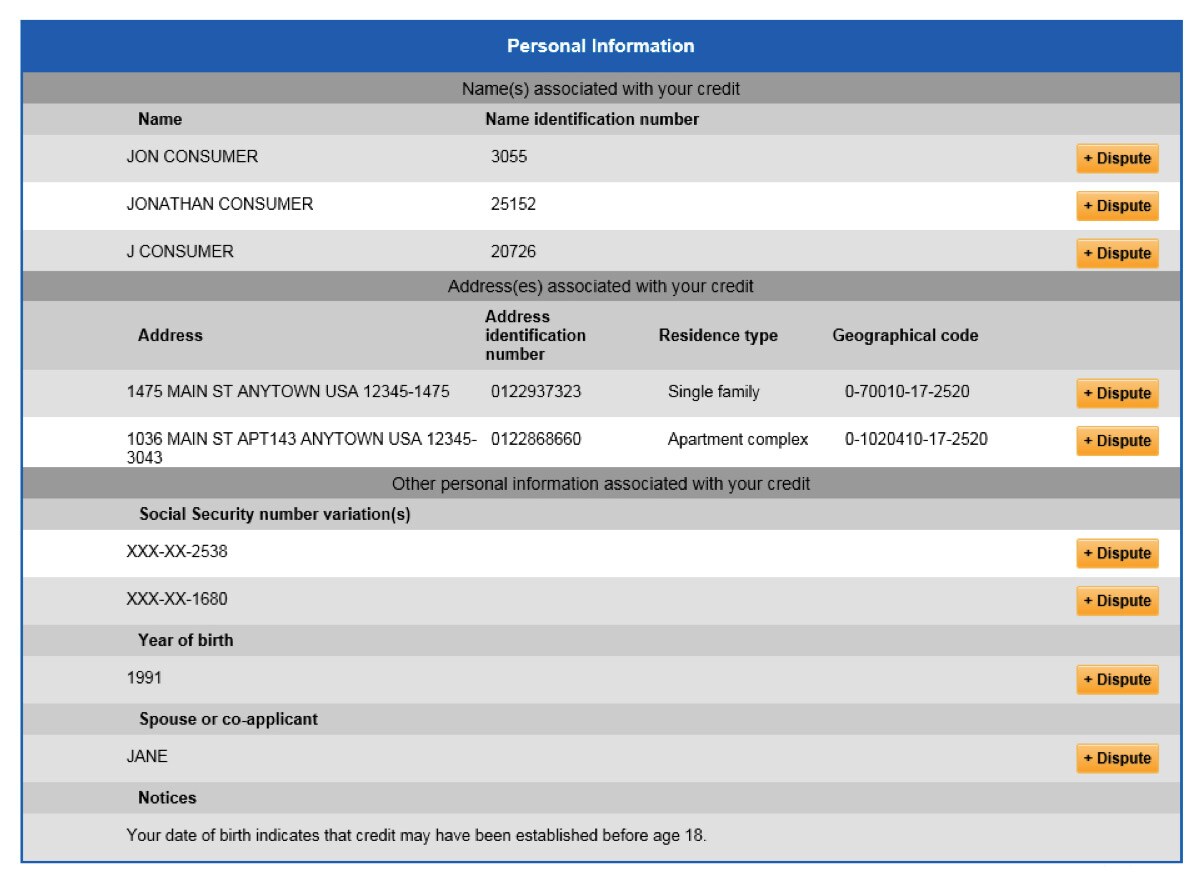

Click the image to see a sample credit report from Experian.

Credit reports contain four main types of information, and you should review all of them for accuracy and completeness. Any credit report errors could affect your credit score, so you want to catch them early.

This first section of your credit report includes personal data such as your name, Social Security number, address, previous addresses, birthdate, and employment history. This information is used to verify your identity rather than affecting your credit score. A mistake in this section could be a simple clerical error, or it could be an indication that your credit file has been compromised or mixed up with someone else’s.

In this section, you’ll find information about open and closed accounts in your name.

Account type: This field shows whether the account is a mortgage, auto loan, credit card, etc.

Account status: This piece shows whether the account is open, closed, in good standing, delinquent, or charged off. If the account’s closed, you’ll also see an estimate of how long it will stay on your credit report.

Opening date: This is the date you opened the account, which is important because the length of your credit history influences your credit score. Typically, a longer credit history has a more favorable impact on your credit score than a shorter history.

Account balance: This line shows how much you currently owe on your account. Combined with your credit limits, the reported amount affects your credit utilization ratio, which can determine up to 30% of your credit score.

Credit limit: If you have revolving accounts (like a credit card, home equity line of credit, or personal line of credit), this field shows the maximum amount of credit you have at your disposal. If you have installment loans (such as a mortgage, auto loan, or student loan), it shows the initial amount you borrowed when you got the loan.

Payment history: This part shows your payment status for each month the account was open. It will indicate if the payment was on time, and identify late or missed payments that were 30, 60, 90, or 120 days or more past due.

Together, this data provides a clear snapshot of how you’ve managed your credit over time. Lenders use this information to assess your financial reliability, so it’s important to regularly review this section for accuracy and to understand how your habits may be influencing your credit score.

This section contains information that’s on public record with state and county courts, including bankruptcies, foreclosures, tax liens, and civil judgments. Accounts that have been sent to a collections agency can also be found here.

This is a list of all the entities that have requested a copy of your credit report, which may include lenders, landlords, employers, and insurance companies. These inquiries may be either “hard” or “soft” pulls, but only you can see the soft ones. A hard inquiry, or hard pull, could lower your credit score by a few points, while a soft credit check does not affect your credit score.

Reading your credit report can feel overwhelming, but understanding this document is key to managing your financial health. Whether you’re preparing to apply for a loan or just want to keep an eye on your credit, following these clear steps can help you confidently navigate your report.

Request your report: Start by obtaining your free credit report from AnnualCreditReport.com. You can choose to request just one report at a time, but getting all three at once lets you compare between credit bureaus.

Verify personal information: Check that your name, address, Social Security number, and employment details are accurate. Errors here could signal identity issues and may impact your credit applications.

Review account information: Look at each listed account — including credit cards, loans, and mortgages — and confirm the details for each. That may include balances, payment history, and account status (open, closed, delinquent). Flag any discrepancies you find.

Check for negative items: Scan for late payments, charge-offs, collections, or bankruptcies. Understand how long each negative mark has been on your report, and note anything that seems incorrect or outdated.

Examine inquiries: Under “Credit inquiries,” review who has accessed your credit and why. Hard inquiries indicate your past credit applications and can slightly lower your score, while soft inquiries don’t affect it at all.

Dispute errors promptly: If you spot inaccuracies, file a dispute with the credit bureau(s) online or in writing. Include documentation to support your claim and monitor the response.

Regularly reviewing your credit report is one of the best habits you can build for long-term financial wellness. By understanding each section and taking swift action when needed, you can protect your credit and make informed financial decisions.

Errors are quite common, and they could falsely impact your credit score. So it’s important to dispute them and try to get them fixed as soon as possible. These mistakes could include an account you didn’t open, inaccurate payment information, an address where you never lived, or something that happened too long ago to still be on your report.

To dispute an error on your credit report, contact the credit reporting agency — or all three if the error appears in all your credit reports. You can submit your dispute online, in writing, or by phone. If possible, you should also contact the party that provided the information in question. The bureaus will conduct investigations and report their findings to you, typically within 30 days.

Once you know how to properly read your credit report, you’ll have a pretty good idea of what the financial world sees when it looks at your profile. You’ll also be able to keep track of your payment history, identify the positive or negative trends, and correct any errors.

Regularly inspecting your credit report is a valuable exercise, but you don’t have to wade through the whole thing every single time. Credit One Bank offers free monthly access to your credit report summary and credit score if you’re a cardmember. You can even see if you pre-qualify without impacting your credit score.

About the author:

Heather ValeHeather is an accomplished writer and editor in the financial and business industries, with expertise in credit building, investments, cryptocurrency, entrepreneurship, and thought leadership. She loves investigating and pulling apart complicated topics to make them simple, engaging, and easy to understand. But she also enjoys writing about the personal side of life, including self-help, creativity, relationships, families, and pets. She approaches everything from a yin-yang perspective, so her passion for wordplay and metaphors is always balanced with an intense focus on accuracy. Heather has a BFA in Visual Arts from York University, and has worked as a journalist in all media: TV, radio, print, and online.

This material is for informational purposes only and is not intended to replace the advice of a qualified tax advisor, attorney or financial advisor. Readers should consult with their own tax advisor, attorney or financial advisor with regard to their personal situations.

Thu Feb 04 2021

If you need to borrow money from a lender (financial institutions like banks or credit unions, not your friends or family), you have two main choices: you can take out a loan or get a

Tue Oct 07 2025

You hear a lot about credit scores, but what exactly are they? Find out what goes into your credit score and why it’s important.

Thu Oct 24 2019

If you’ve had any experience with credit, you’ve probably heard the term “credit bureau.” It may have been when a potential lender informed you they were going to pull your credit