Tue Apr 21 2026

Denied by a Number: The Hidden Cost of Poor Credit

Poor credit can lead to denials, and that may lead to even more complications. Not all of them are what you’d expect.

FDIC-Insured - Backed by the full faith and credit of the U.S. Government

July 07, 2026

What would encourage you to move your money to a different bank? Nearly half of U.S. consumers say a better interest rate is key.

In this article:

For most of modern banking history, where you kept your savings was a decision you made once and rarely revisited. Switching felt like more trouble than it was worth, and banks built their retention strategy on that inertia.

That era is over. A new Credit One Bank survey of 1,000 U.S. consumers found that nearly 48% of U.S. consumers moved at least some of their savings in the past year to earn a higher annual percentage yield (APY). Specifically, more than 19% moved most of their savings, while over 28% moved some.

This implies a fairly widespread willingness to move money for a better return. The rate-shopping behavior that banks once treated as an outlier habit is now more mainstream, and those doing it aren’t necessarily the ones anyone expected.

Awareness seems to be driving this shift more than anything else. With the national average savings account paying just 0.38% APY while top high-yield accounts advertise rates near 4.10%, the cost of staying put has become hard to ignore. People know the gap exists and they know it’s pretty big. As a result, more of them are acting on it.

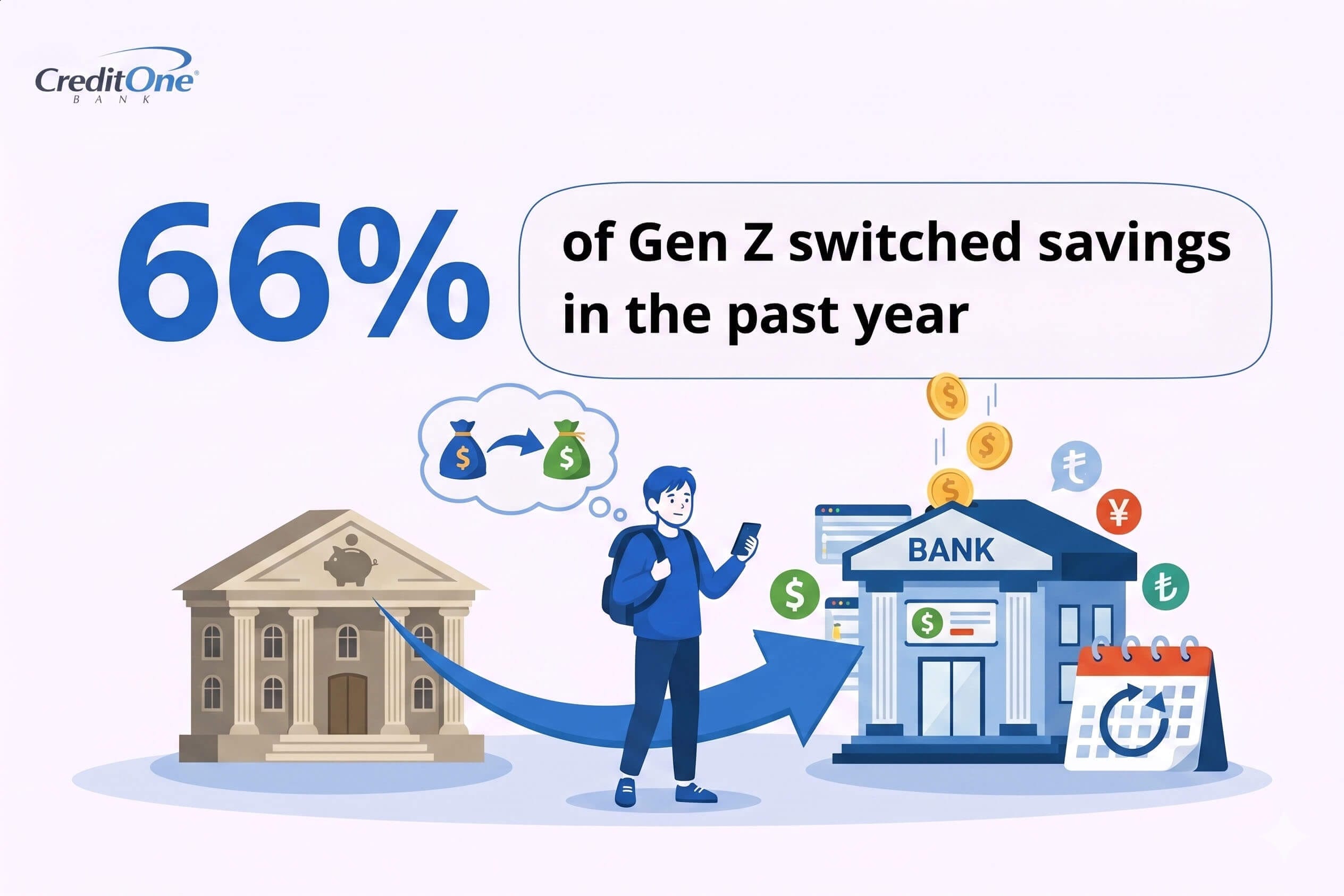

Nearly 48% of U.S. consumers moved at least some savings in the past 12 months to get a better APY; among Gen Z, that figure jumps to almost 66%.

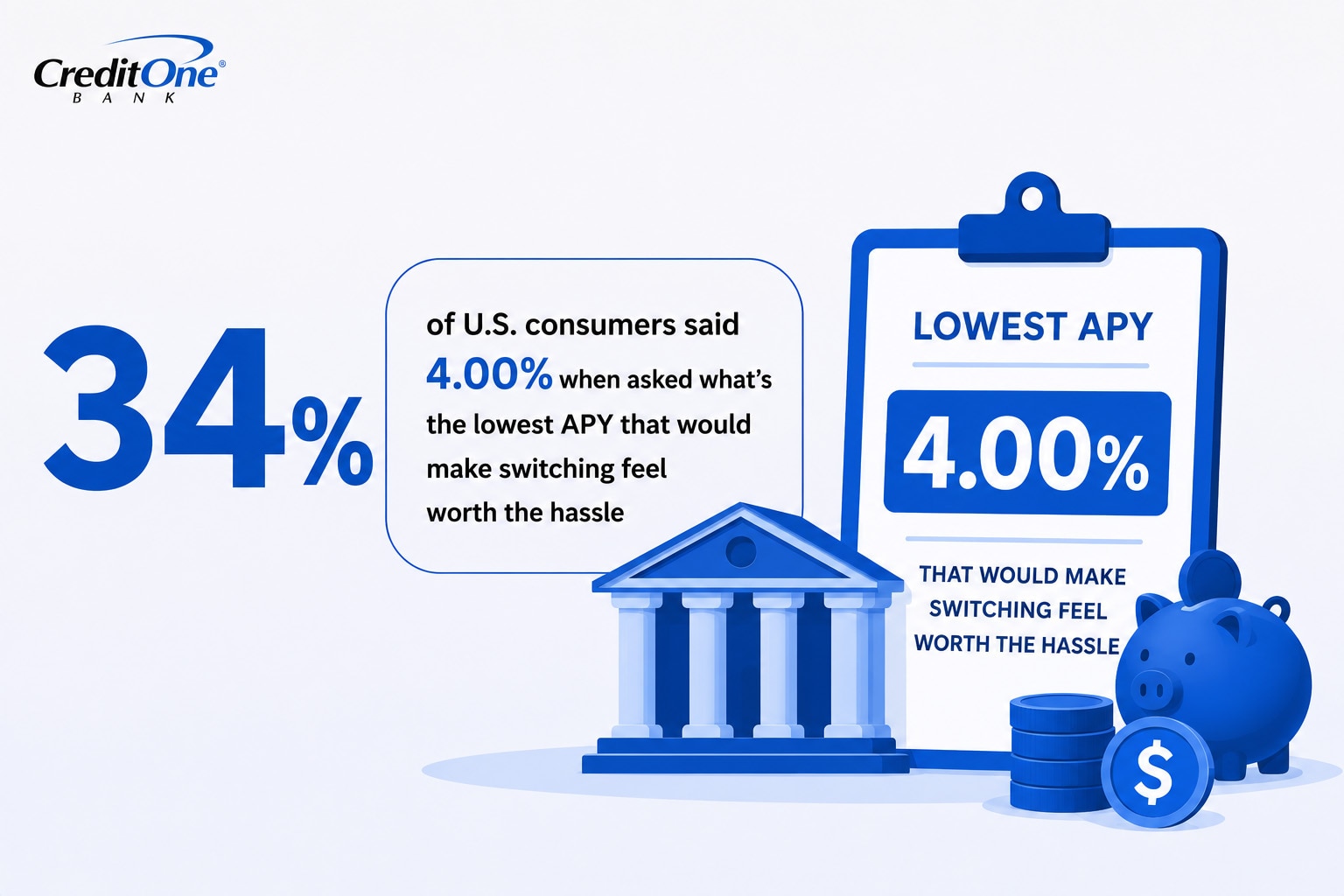

4.00% is the most common minimum APY that makes switching feel worth it as cited by nearly 34% of respondents.

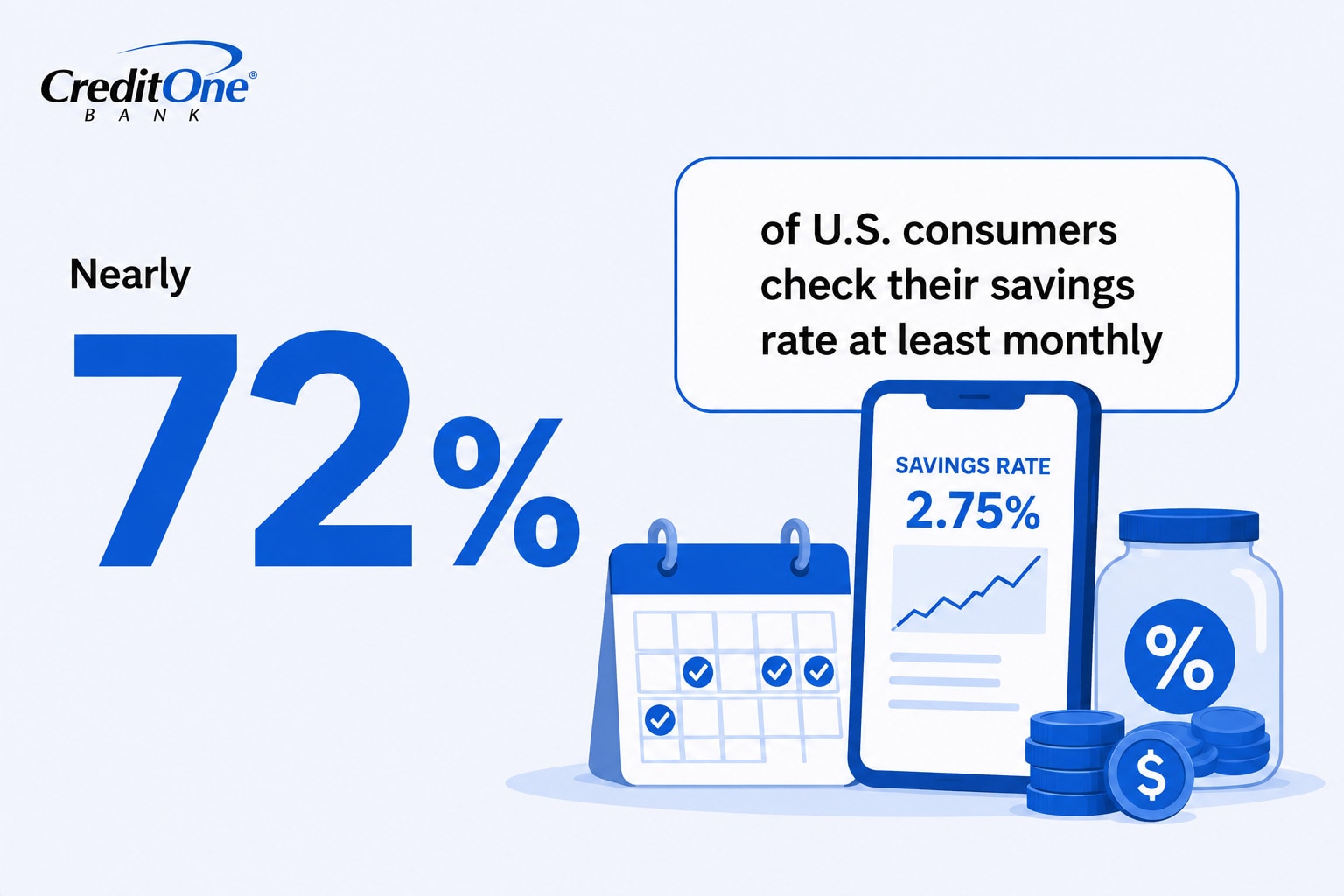

Almost 72% of U.S. consumers now check their savings APY at least monthly, with close to 38% of Gen Z checking weekly or more.

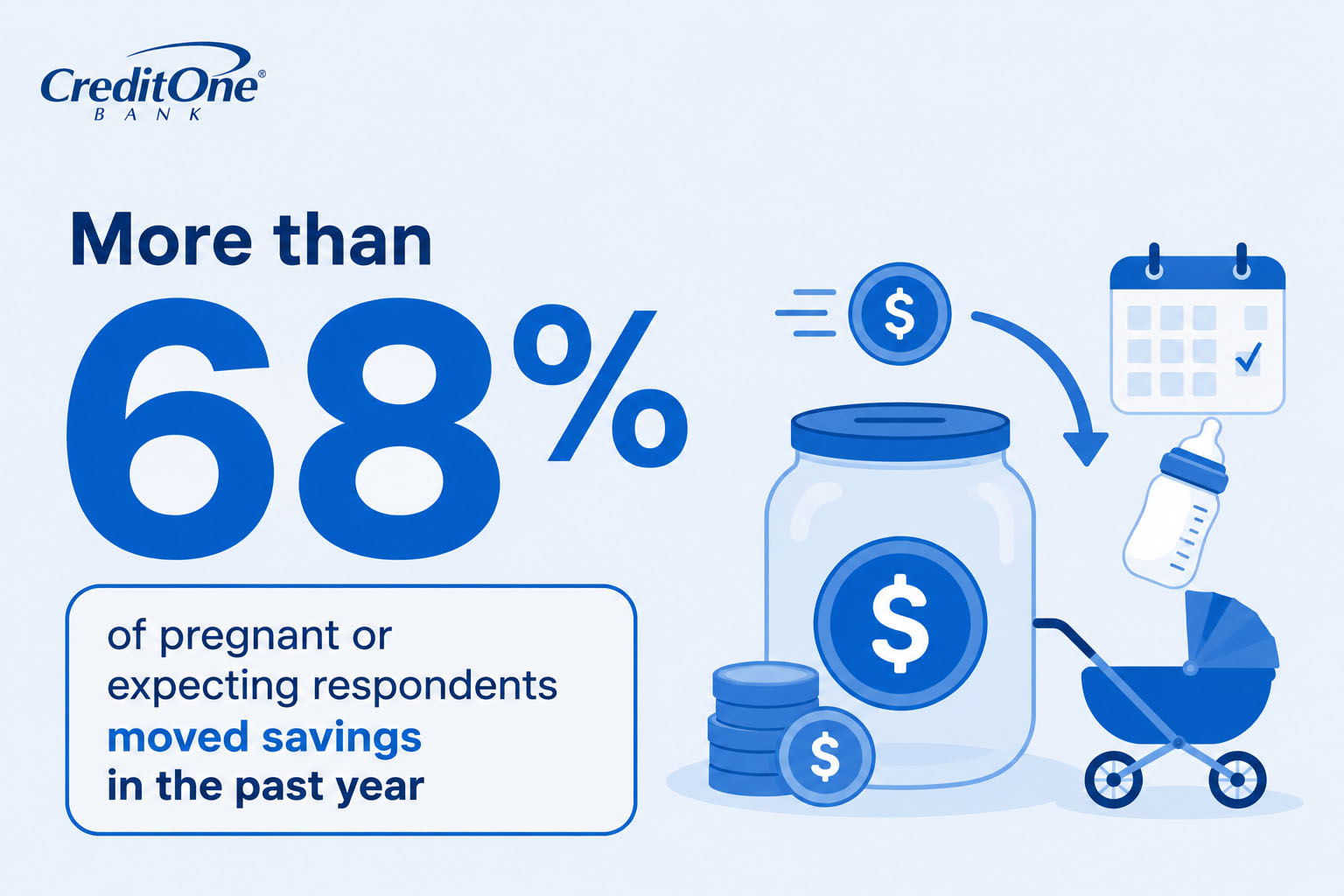

More than 68% of pregnant or expecting respondents moved savings in the past year, which is the highest of any group surveyed.

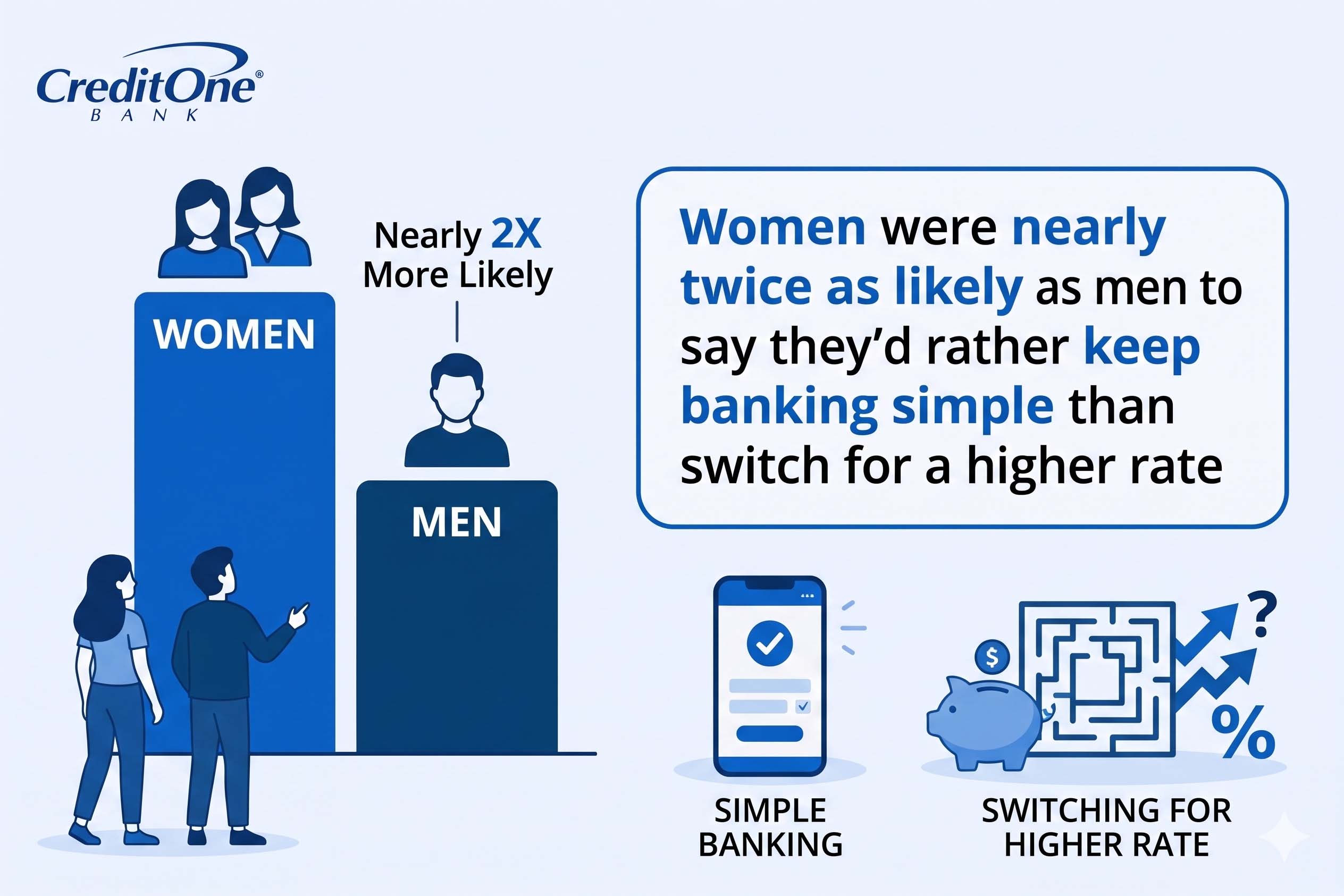

Over 21% of women say they’d rather keep banking simple than switch for a higher rate — nearly double the 11% of men who say the same.

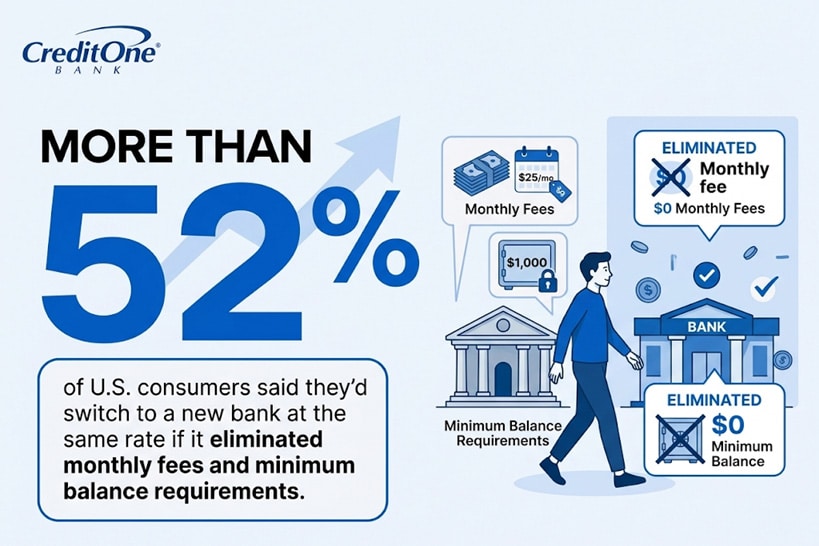

More than 52% would switch to a new bank at the same APY for no monthly fees, the single most powerful non-rate motivator.

Almost 45% say a sign-up bonus would motivate a switch, nearly matching fee elimination and rising to 50% among baby boomers.

For years, the customer considered most likely to move money for a better deal fit a familiar profile: financially established, attentive, and probably older. But the new data flips that assumption. Among Gen Z, nearly 66% switched savings in the past year, with over 19% moving most of their money and the rest moving some. Baby boomers were the most reluctant to budge, with less than 31% making any move at all.

The reason comes down to how each generation experiences money. Gen Z banks on its phone — across national surveys, roughly nine in ten use financial apps, and about two-thirds reach for a mobile app first, so moving money is a few taps rather than a trip to a branch. But baby boomers grew up when switching banks meant paperwork and lost relationships, so less than 40% bank by app and nearly a quarter avoid them for financial tasks.

Because of this, banks that assume older customers are most likely to leave might be focusing their retention strategies on the wrong demographic.

If there’s a single figure that defines the moment, it’s 4.00%. When asked the lowest APY that would make switching feel worth the hassle, nearly 34% of U.S. consumers landed there, and it was the most common answer by a wide margin. Gen Z aligned closely at more than 39%. The threshold tracks almost exactly with what the best accounts in the market actually pay right now, which puts the trigger point within reach for a large share of savers.

The picture changes among the highest earners and oldest savers. Among those making $250K or more, over 33% need 4.50% or higher and another 33% need 5.00% or more before considering a move. Baby boomers set a similar bar: 25% require 5.00% or higher before they’ll act, and nearly 10% say they’d never switch for a rate at all.

However, the 4.00% line represents a good balance — low enough to be real and high enough to matter. CD-rate experts expect yields to hold steady through summer 2026, with top accounts hovering between 4.10% and 4.15%, so the threshold isn’t going anywhere. For banks paying anything close to the 0.38% national average, that’s the type of gap their customers are measuring them against.

Nearly 72% of U.S. consumers check their savings rate at least monthly, and close to 38% of Gen Z check weekly or more. That level of vigilance didn’t exist before comparison tools made it almost effortless.

Two things explain the shift. The first is that watching now pays off in a way it didn’t a decade ago. The top high-yield accounts run about ten times the 0.38% national average, which on a $25,000 balance is the difference between earning roughly a thousand dollars a year and less than a hundred. Through the near-zero years of the early 2020s, when the best rates sat between 0.50% and 1.50%, there was little reason to look elsewhere.

The second reason is that looking got easier, as mobile banking and rate-tracking tools turned passive numbers into something people can check in seconds. Boomers remain the outliers, with almost 33% checking just a few times across six months. However, even that’s still more engaged than some stereotypes might suggest.

The consequence for banks is that rate cuts are quickly noticed when customers look at the data regularly. The window between the rate dropping and the customer knowing about it has shrunk from months to days, and that change reshapes how quickly they might leave.

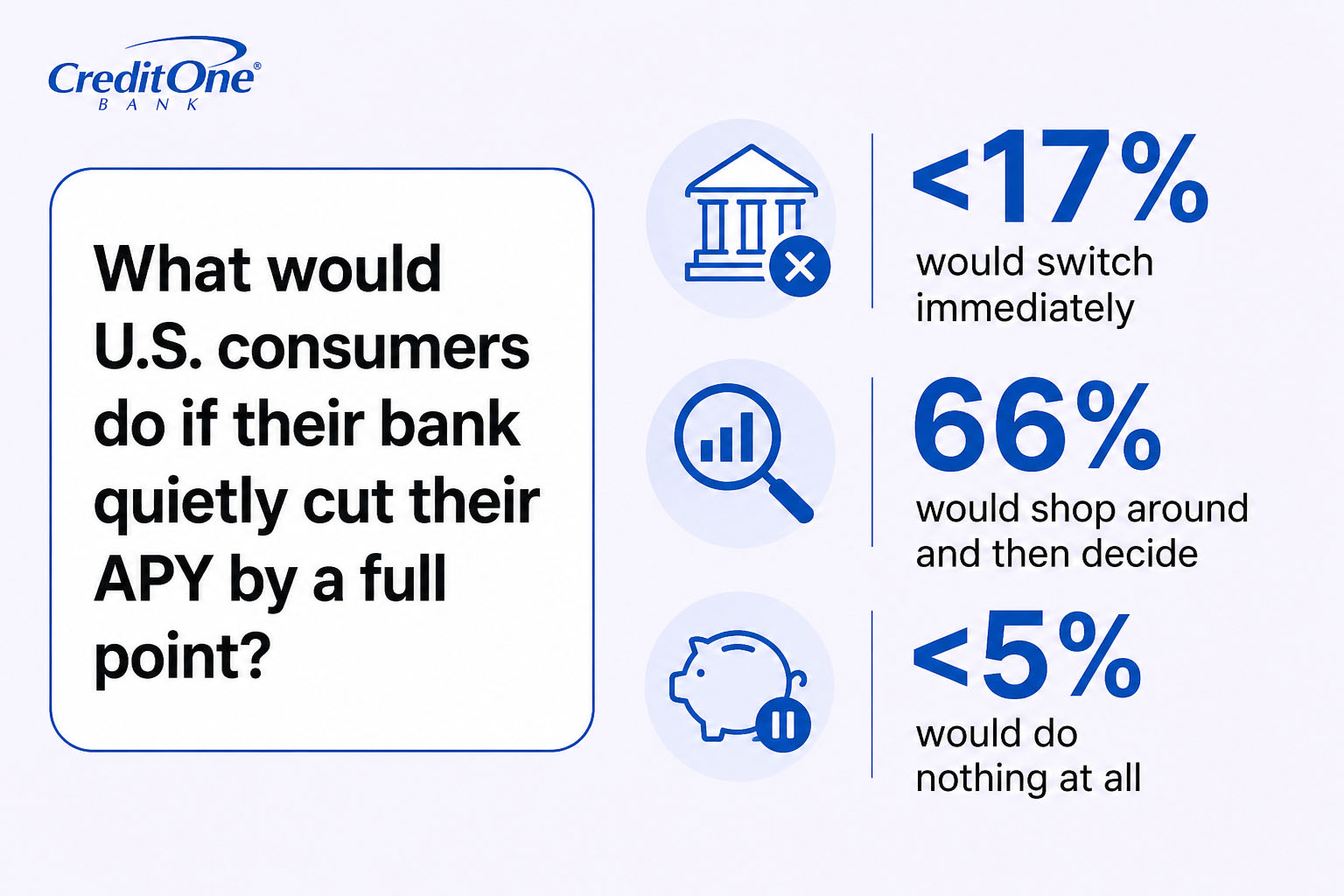

If their bank quietly cut their APY by a full point, less than 17% of U.S. consumers would switch immediately. At face value, that looks reassuring for the bank. But 66% said they’d shop around and then decide, and less than 5% would do nothing at all.

The mistake banks make is assuming that customers are happy just because they haven’t left yet. Two-thirds of customers respond to a rate cut by actively comparing alternatives, so a large group of people are just one good offer away from jumping ship. A customer who stays put after a rate cut isn’t necessarily loyal if they’re actively looking for alternatives.

Instead, that customer who’s shopping around may have effectively decided to leave as soon as they find somewhere better. And since the average bank pays a fraction of what top accounts offer, it’s relatively easy to find a greener pasture.

Family status turns out to be a strong predictor of rate-chasing behavior, and the most active movers are people preparing for or raising children. Respondents with kids under 18 optimized their finances by moving money and monitoring rates at consistently elevated levels.

But the standout group is a subset within that broader parental population. Pregnant and expecting respondents posted the most aggressive numbers anywhere in the survey, and parents of young children weren’t far behind.

More than 68% of pregnant or expecting respondents moved savings in the past year, which is the highest of any group measured, against less than 48% of all respondents.*

Nearly 54% of respondents with kids under 18 moved savings, which is also well above the national figure.

Just over 34% of pregnant or expecting respondents would switch banks immediately if their rate were cut by a point — again the highest share of any group.

Intuitively, the behavior makes sense. A baby on the way tends to sharpen financial decisions, and a few tenths of a percent on emergency savings is more of a motivator when there’s a nursery to fund.

So while banks might treat this life stage as a moment to deepen loyalty, with a new family and new accounts, it’s not a good assumption to make. By contrast, this is the exact moment customers are most willing to walk.

Women were nearly twice as likely as men to say they’d rather keep banking simple than switch for a higher rate, at just over 21% versus 11%. And the rest of the data paints a fuller picture of what that means.

Women were more likely to prioritize instant access to emergency savings (just over 38% versus 30% of men) and less likely to rank the highest possible rate as their top concern (less than 26% versus 38% of men).

This pattern shows that chasing a higher APY isn’t always the goal. With women ranking “rate” below liquidity and stability, banks that try to woo them with numbers aren’t exactly speaking to their priorities or values.

But banking isn’t just about interest rates. So when the APY is identical, what actually makes a customer switch? The clear winner is the absence of fees. More than 52% of U.S. consumers said they’d switch to a new bank at the same rate if it eliminated monthly fees and minimum balance requirements. That beat out a great mobile app (almost 41%), 24/7 service (38%), and branch locations (37%).

A close runner-up is the sign-up bonus. Nearly 45% said a promotional offer would move them, and the figure climbs to 50% among baby boomers. That puts bonuses on nearly equal footing with fee elimination, which suggests they function as more than a one-time acquisition cost in consumers’ decisions.

Taken together, the findings point to a sequence. Rate determines whether a bank gets considered at all, and the factors beyond rate determine whether a customer actually switches. Once an account clears the 4.00% bar, fee structure and the rest of the package help make the decision.

The shift in banking attitude is about visibility more than anything else. For decades, the gap between what the average bank paid and what savers could earn elsewhere was fairly wide but easy to miss. Few people checked their rate, fewer compared it against other options, and most stayed where they were by default. That rate gap hasn’t closed, but people can see it now, and the tools to act on it often take just seconds to use.

The groups leading the change — from Gen Z checking rates weekly to parents moving money before a baby arrives to women weighing stability against yield — are taking advantage of technology. They have better information and easier tools than savers did 10 to 20 years ago, and they’re using both.

For banks, the implication is straightforward. A fair rate and no hidden fees are now the baseline customers expect, and loyalty can’t be taken for granted. With two-thirds of customers willing to shop around the moment their rate drops, keeping them takes more than assuming they’ll stay.

Find the full survey and responses here.

To understand how U.S. consumers approach saving, switching banks, and locking in guaranteed returns, we surveyed 1,000 adults across the country who are familiar with savings account interest rates and certificates of deposit (CDs). Participants answered a series of questions about what minimum APY would prompt them to switch banks, how closely they monitor their savings rates, how they’d respond to a rate cut, and what non-rate factors would motivate a move.

Responses were analyzed by demographic groups, including age, gender, household income, education, ethnicity, and parental status, to identify trends and disparities. Some demographic subgroups represent smaller sample sizes; where those figures appear, they are presented as directional rather than statistically definitive.

*The pregnant or expecting cohort is a small subgroup of roughly 41 respondents, so these figures are directional rather than precise. The broader pattern among parents, drawn from far larger samples, is the more reliable signal.

Readers are welcome to utilize the insights and findings from this study for non-commercial purposes, such as academic research, educational presentations, and personal reference. When referencing or citing this article, please ensure proper attribution to maintain the integrity of the research. Direct linking to this article is permissible, and access to the original source of information is encouraged.

For commercial use or publication purposes, including but not limited to media outlets, websites, and promotional materials, please contact the authors for permission and licensing details. We appreciate your respect for intellectual property rights and adherence to ethical citation practices. Thank you for your interest in our research.

This material is for informational purposes only and is not intended to replace the advice of a qualified tax advisor, attorney or financial advisor. Readers should consult with their own tax advisor, attorney or financial advisor with regard to their personal situations.

Tue Apr 21 2026

Poor credit can lead to denials, and that may lead to even more complications. Not all of them are what you’d expect.

Wed Jun 10 2026

Would you leave your money untouched for a fixed term if it meant earning a higher return? Here’s what U.S. consumers said about it.

Thu May 28 2026

How do you look at credit cards compared to your peers and parents? Find out what consumers said in our new survey.