Tue Feb 10 2026

Groceries, Debt and Doubt: The Financial Mood of U.S. Consumers Heading Into 2026

We surveyed 1,000 people to find out how rising costs, lack of savings and income uncertainty may be shaping personal finances in 2026.

FDIC-Insured - Backed by the full faith and credit of the U.S. Government

April 21, 2026

Poor credit can lead to denials, and that may lead to even more complications. Not all of them are what you’d expect.

In this article:

When a financial institution says no, the consequences rarely end with one declined application. A new survey of 1,000 U.S. consumers who have experienced a credit-based denial shows how deeply that moment can ripple through someone’s life.

Credit scores now influence far more than loan approvals. They shape access to rental housing, auto financing, insurance policies, utilities, and more. As a result, that little three-digit number can influence opportunity, timing, and even self-confidence.

80% say credit-based denials have negatively affected their confidence or self-esteem

23% have given up on a major life milestone because of a credit denial

51% say poor or limited credit has cost them $2,000 or more over their lifetime

62% were surprised to learn they were denied

54% waited seven months or longer before applying for credit again

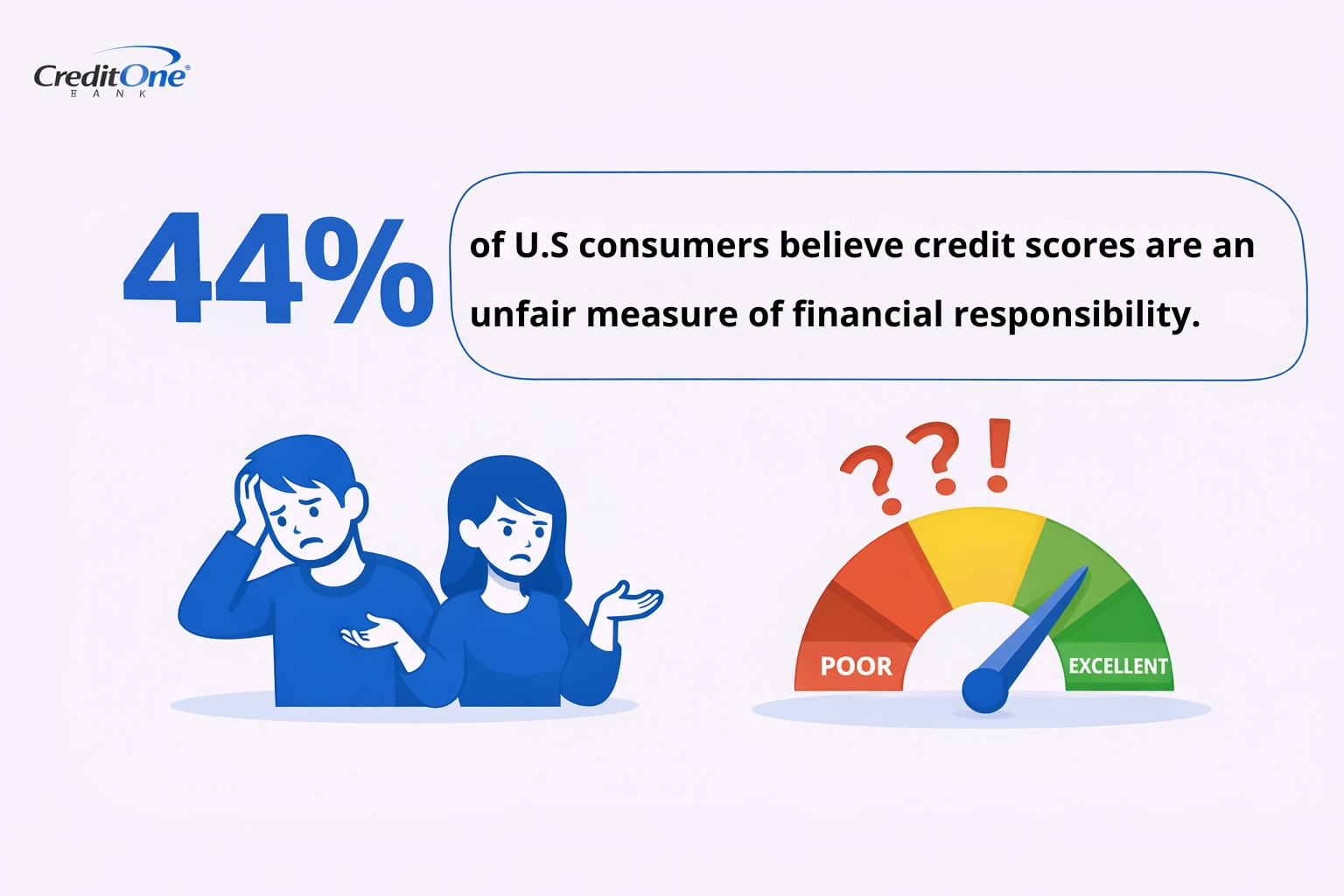

44% believe credit scores are an unfair way to measure financial responsibility

46% had to borrow from family or friends after being denied

For many U.S. consumers, a denial for credit feels personal. 80% of respondents say being turned down hurt their confidence or self-esteem. The emotional impact is even sharper among women, with 63% reporting stress or anxiety after a denial, compared to 50% of men.

Credit scores are about loan risk, but they can also determine who qualifies for housing, what they pay for car insurance, and how they get access to other essentials.

When the approval criteria feel unclear, and the stakes are high, rejection can feel like a judgment of character rather than just a numerical calculation. The system might be based on technical data, but people’s reactions are entirely human.

The financial consequences also extend well beyond one application. More than half of respondents say poor or limited credit has cost them at least $2,000 over time. And nearly one in three millennials report even higher losses of $5,000 or more.

These costs might not be immediately obvious, but even small differences in interest rates can add up over time. And when traditional lenders decline an application, the alternatives often come with even higher rates, not to mention larger deposits. So access to credit doesn’t necessarily disappear, but it does become a lot more expensive.

As a result, many people turn to personal connections instead, with nearly half saying they borrowed from family or friends after being denied credit.

Credit is often the bridge to major life goals. And because of that, nearly one in four respondents say they gave up on a personal milestone, like buying a home, starting a business, or getting married, after being turned down for a loan.

That finding comes at a time when housing affordability is uncertain and costs of borrowing are increasing. Younger adults are already navigating rising rents and competitive real estate markets. A barrier to credit can quickly push their plans further out of reach.

As a result, a home purchase may get postponed, a business idea might sit on hold, and a major goal can shift from “this year” to “someday.”

One of the most revealing insights from the survey is that the majority of people did not see it coming. 62% say they were surprised by their denial.

Credit scoring models are complex, and different lenders may rely on different versions. Each one is based on slightly different criteria, so small shifts in payment history or credit utilization can influence outcomes in ways consumers may not anticipate.

That disconnect often leads to doubt, and nearly 44% believe credit scores are an unfair measure of financial responsibility. But their frustration is likely more about lack of clarity than the concept of credit itself. If a number influences so many aspects of their lives, many U.S. consumers want a clearer understanding of how it works.

After a denial, many people take a step back. More than half waited seven months or longer before applying for credit again. That’s understandable, because rejection often causes hesitation. And waiting between applications can also be a good credit-building strategy.

But the data shows another response as well. Among Millennial U.S. consumers, 33% say being denied motivated them to improve their credit. And 21% of Gen Z respondents report working with a financial advisor to strengthen their credit.

Financial literacy resources and credit monitoring tools are more accessible than ever, so it’s easier for consumers to shift their mindset from avoidance to awareness. The system might feel big and impersonal, but that doesn’t mean people are walking away from it.

Credit scores remain a powerful gatekeeper in modern financial life. They can influence who rents an apartment, who qualifies for loan financing, and who moves forward with long-term plans.

The survey findings reveal how heavy that influence can feel for many consumers. Higher overall costs might be expected, but it can also lead to lower confidence and the decision to put off major milestones.

At the same time, something else is happening. Many U.S. consumers are choosing to learn the rules of the system rather than disengage from it. They’re not just responding to rejection with frustration — it also motivates them to be more curious and work toward regaining control.

That line in the sand between feeling judged and wanting to change the situation might define the modern credit experience more than any number ever could. And when people become more determined to understand it, manage it, and move forward anyway, a credit score on the lower end of the scale can actually highlight opportunity instead of standing in the way.

Find the full survey and responses here.

To understand how U.S. consumers experience credit-based denials, we surveyed 1,000 adults across the country who have been denied a financial product or service because of their credit score. Participants answered a series of questions about the type of denial they faced, the financial consequences that followed, and the emotional impact of that experience. Responses were analyzed by demographic groups, including age, gender, income, and race, to identify trends and disparities in how credit denials affect different populations.

Readers are welcome to utilize the insights and findings from this study for noncommercial purposes, such as academic research, educational presentations, and personal reference. When referencing or citing this article, please ensure proper attribution to maintain the integrity of the research. Direct linking to this article is permissible, and access to the original source of information is encouraged.

For commercial use or publication purposes, including but not limited to media outlets, websites, and promotional materials, please contact the authors for permission and licensing details. We appreciate your respect for intellectual property rights and adherence to ethical citation practices. Thank you for your interest in our research.

This material is for informational purposes only and is not intended to replace the advice of a qualified tax advisor, attorney or financial advisor. Readers should consult with their own tax advisor, attorney or financial advisor with regard to their personal situations.

Tue Feb 10 2026

We surveyed 1,000 people to find out how rising costs, lack of savings and income uncertainty may be shaping personal finances in 2026.

Mon Dec 08 2025

Many people think they know a lot about credit. But as it turns out, there may be some crucial knowledge gaps among consumers.

Mon Oct 20 2025

What’s in a number? Find out how adults from two distinct generations factor in credit scores and financial habits as they assess relationships.