Tue Apr 21 2026

Denied by a Number: The Hidden Cost of Poor Credit

Poor credit can lead to denials, and that may lead to even more complications. Not all of them are what you’d expect.

FDIC-Insured - Backed by the full faith and credit of the U.S. Government

May 28, 2026

How do you look at credit cards compared to your peers and parents? Find out what consumers said in our new survey.

In this article:

For most of their history, credit cards served a narrow purpose. Consumers used them for large or unexpected purchases, not for buying coffee or groceries. That changed in 1986 when Sears launched the Discover Card with a radical idea: “Cashback Bonuses” on every purchase.

The concept transformed plastic from an emergency tool into an everyday spending companion, and other issuers followed. By the 1990s, rewards programs, airline miles, and point systems had become standard. The baby boomer generation built their credit habits around this new reality, trained to see their cards as vehicles for earning something back on every swipe.

That rewards-first mindset stuck. But the latest generation of cardholders never inherited it. A new Credit One Bank survey of 1,000 U.S. consumers who hold at least one personal credit card shows how far the generational gap has widened.

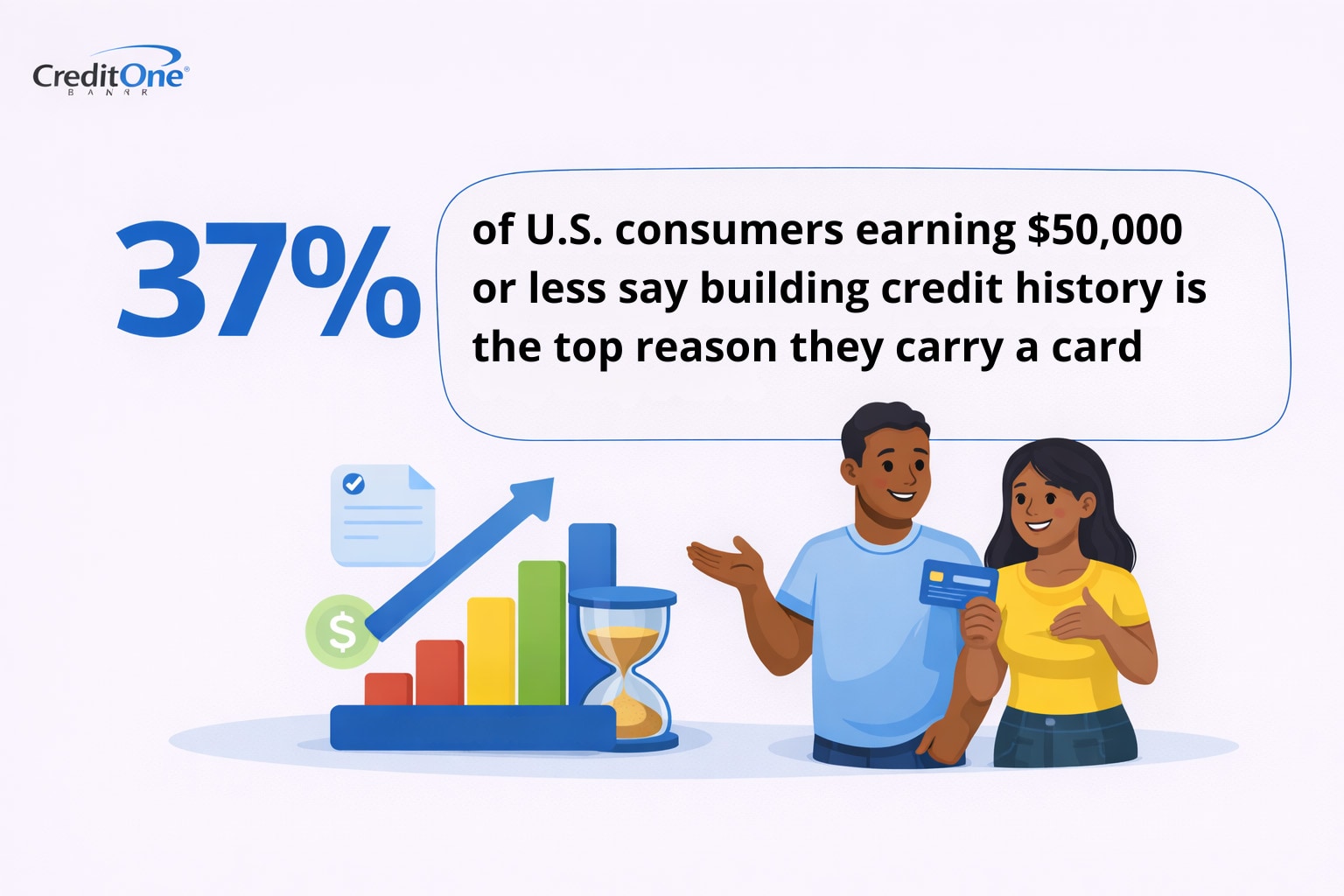

While older, higher-earning consumers treat their cards as reward engines, with 38% of those making $150,000 or more citing cash back and points as their primary motivator, younger and lower-income cardholders have a different priority. Among those earning $50,000 or less, 37% say building credit history or score is the top reason they carry a card.

So while boomers typically use a credit card to earn a return on spending, Gen Z may see it as an investment in financial access. That divide is reshaping how card issuers think about their products, their marketing, and their relationship with customers across age groups.

37% of U.S. consumers earning $50,000 or less say their primary reason for using a credit card is building credit history or score.

49% of U.S. consumers say their credit card usage has increased over the past two years.

77% say carrying a credit card balance month to month creates anxiety for them.

60% of millennials carried a balance on their credit card at least once in the past 12 months, the highest rate of any generation.

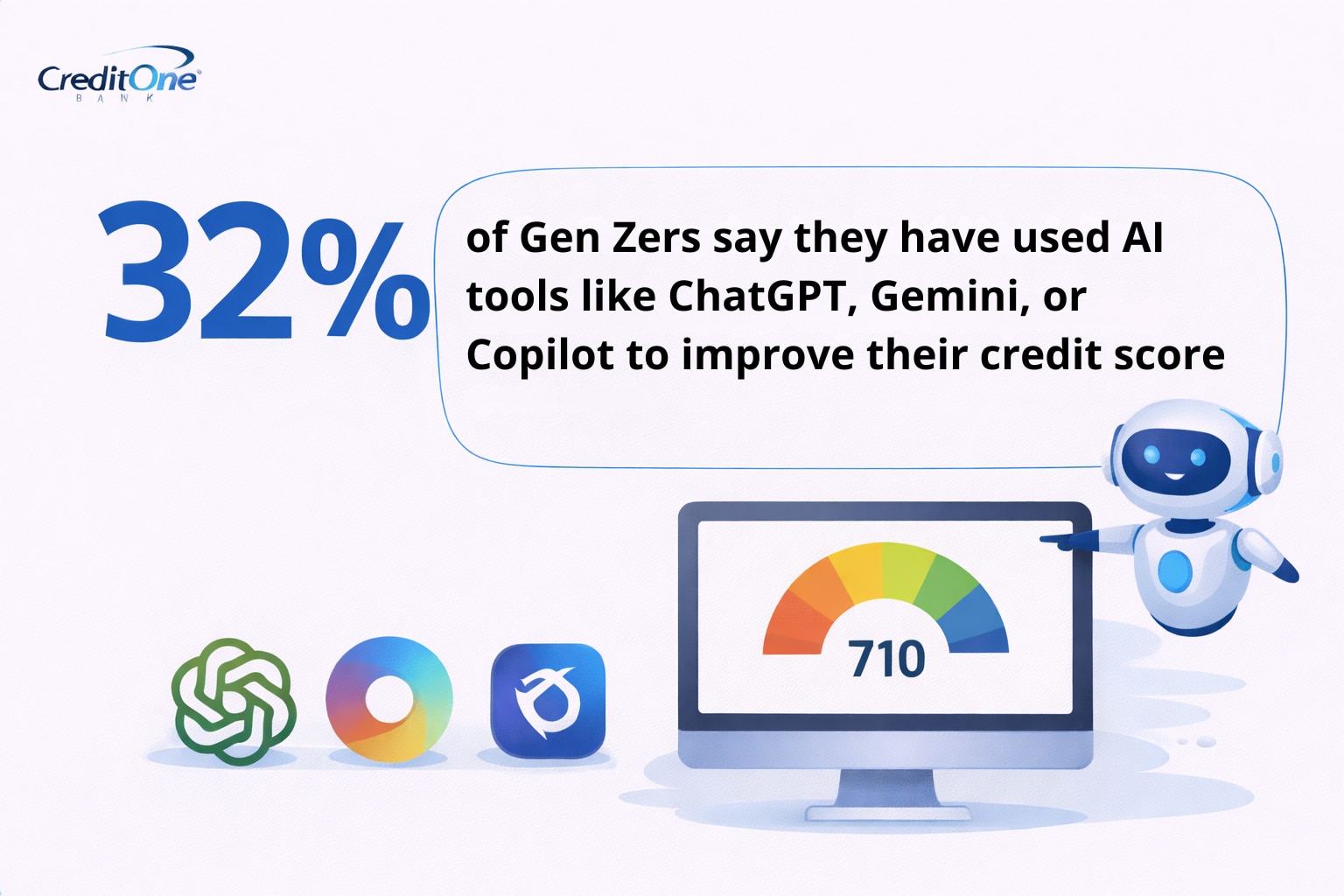

32% of Gen Zers have used AI tools to improve their credit score.

68% of U.S. consumers say cash back is a very appealing reward option for their main credit card.

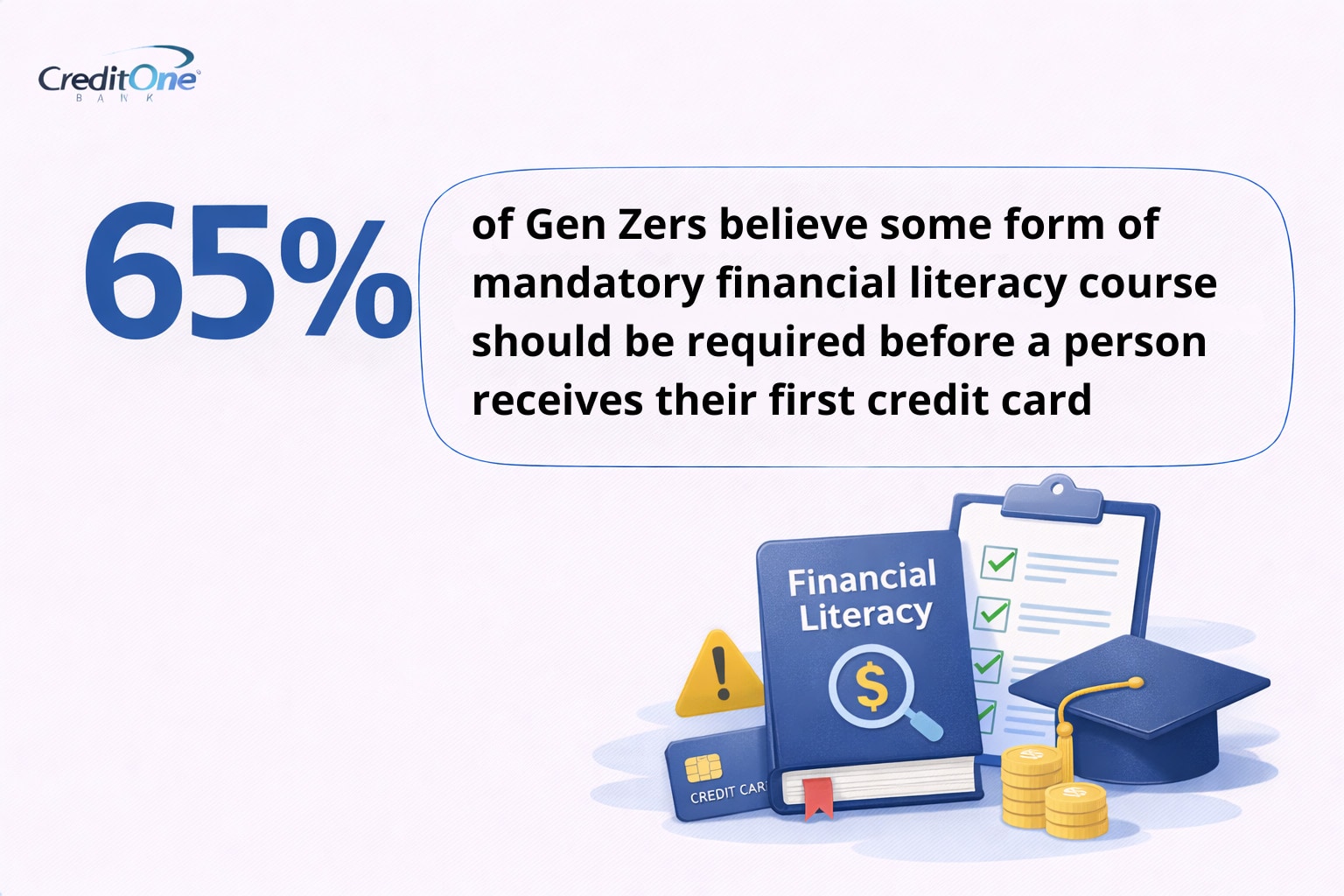

65% of Gen Zers believe some form of mandatory financial literacy course should be required before getting a first credit card.

The traditional credit card pitch centers around what you earn by spending. Like points for flights, cash back on groceries, and bonus categories that rotate each quarter.

And that pitch resonates with consumers who grew up during the rewards era and already have established credit profiles. For them, the card is a tool for maximizing the value of money they’re already spending.

But for younger Gen Z consumers, many of whom are still establishing their financial identities, the credit card is a stepping stone toward financial access — from better rates on auto loans to qualifying for a mortgage.

The same pattern is true across income lines: 37% of U.S. consumers earning $50,000 or less say building credit history is the top reason they carry a card. And a practically identical proportion (38%) of those earning $150,000 or more say rewards and cash back drive their card use instead.

So the generational and income divides run parallel. One group needs credit access while the other already has it and wants to maximize returns.

Nearly half of all U.S. consumers (49%) say their credit card usage has increased over the past two years. That number isn’t evenly distributed, though. Among men, 56% report higher usage, compared to only 42% of women.

The rise in usage reflects broader economic pressures. Inflation has pushed everyday expenses higher, and wages haven’t kept up for many households. When the gap between income and cost of living widens, credit fills the space.

The gender difference in increased usage suggests that spending patterns, financial roles within households, or comfort levels with revolving debt may differ between men and women in measurable ways.

More than three-quarters (77%) of U.S. consumers say carrying a credit card balance from month to month creates anxiety for them. That figure is striking on its own, but it gets more complicated when paired with the reality that 60% of millennials did carry a balance at least once in the past year — the highest percentage of any generation. Gen X followed closely at 59%, Gen Z came in at 52%, and boomers at only 37%.

The takeaway is that a large portion of consumers are doing something with their credit cards that actively stresses them out. Millennials, now in their early 30s to mid-40s, are most likely in peak spending years for housing, childcare, and daily living expenses. They feel the tension between financial obligation and financial anxiety more than any other group. Older members of this generation were newly navigating adulthood during the 2008 recession and may have carried that wariness forward.

External data confirms the weight of this burden. Bankrate’s 2026 Credit Card Debt Report found that 48% of people carrying credit card debt have no plan to pay it off. Nearly two in three debtors reported delaying or avoiding financial decisions because of their balances, including saving for emergencies (34%) and investing (23%).

Where older generations relied on bank advisors or family members for financial guidance, Gen Z is turning to AI. Not surprisingly, 32% of Gen Zers say they’ve used AI tools like ChatGPT, Gemini, or Copilot to improve their credit score. Across all ages, 21% of U.S. consumers have used AI for budgeting or spending analysis, and another 21% for credit score improvement.

This shift reflects how modern consumers don’t have to wait for a scheduled appointment at a branch office or a phone call with a customer service rep. Gen Zers prefer immediate, personalized answers, and they’re finding them through AI.

The data also shows that 47% of U.S. consumers are willing to let algorithms play a larger role in personal finance, stating that they’d be comfortable with their card issuer using AI to adjust their credit limit or APR in real time based on spending and risk data.

When asked about reward preferences, 68% of U.S. consumers say cash back is very appealing for their main credit card. It is the top reward type by a wide margin. Flat-rate cash back on everything scored 51% under the “very appealing” option, and higher cash back in fixed categories (such as groceries or gas) earned the same.

Travel-focused rewards tell a different story. 30% of U.S. consumers say co-branded airline and hotel miles are not appealing at all as a reward option. Travel points with bonuses on travel and dining also showed weaker appeal, with only 32% calling them “very appealing.”

So consumers seem to be gravitating toward simplicity and flexibility. Cash back may be is easy to understand, easy to use, and typically doesn’t require predefined travel behaviors or loyalty to a specific airline or hotel chain.

When asked about the importance of knowledge, 65% of Gen Zers believe some form of mandatory financial literacy course should be required before a person receives their first credit card. And 65% of all U.S. consumers agree that credit card companies should market differently to different age groups.

These numbers suggest a generation that recognizes the stakes. Gen Z has watched older siblings, friends, and parents struggle with debt. They see the system clearly enough to know they may need better tools before jumping in. Their support for financial education shows desire for a more transparent entry point that lets them understand the rules before they start playing.

Policymakers are listening. According to the National Endowment for Financial Education, 29 states now require a financial literacy course for high school graduation, up from a handful a decade ago. In 2025 alone, Kentucky, Colorado, Texas, and Delaware all passed new financial literacy graduation requirements.

At the federal level, the Young Americans Financial Literacy Act has been introduced in Congress to fund financial education programs for people aged 8 through 24.

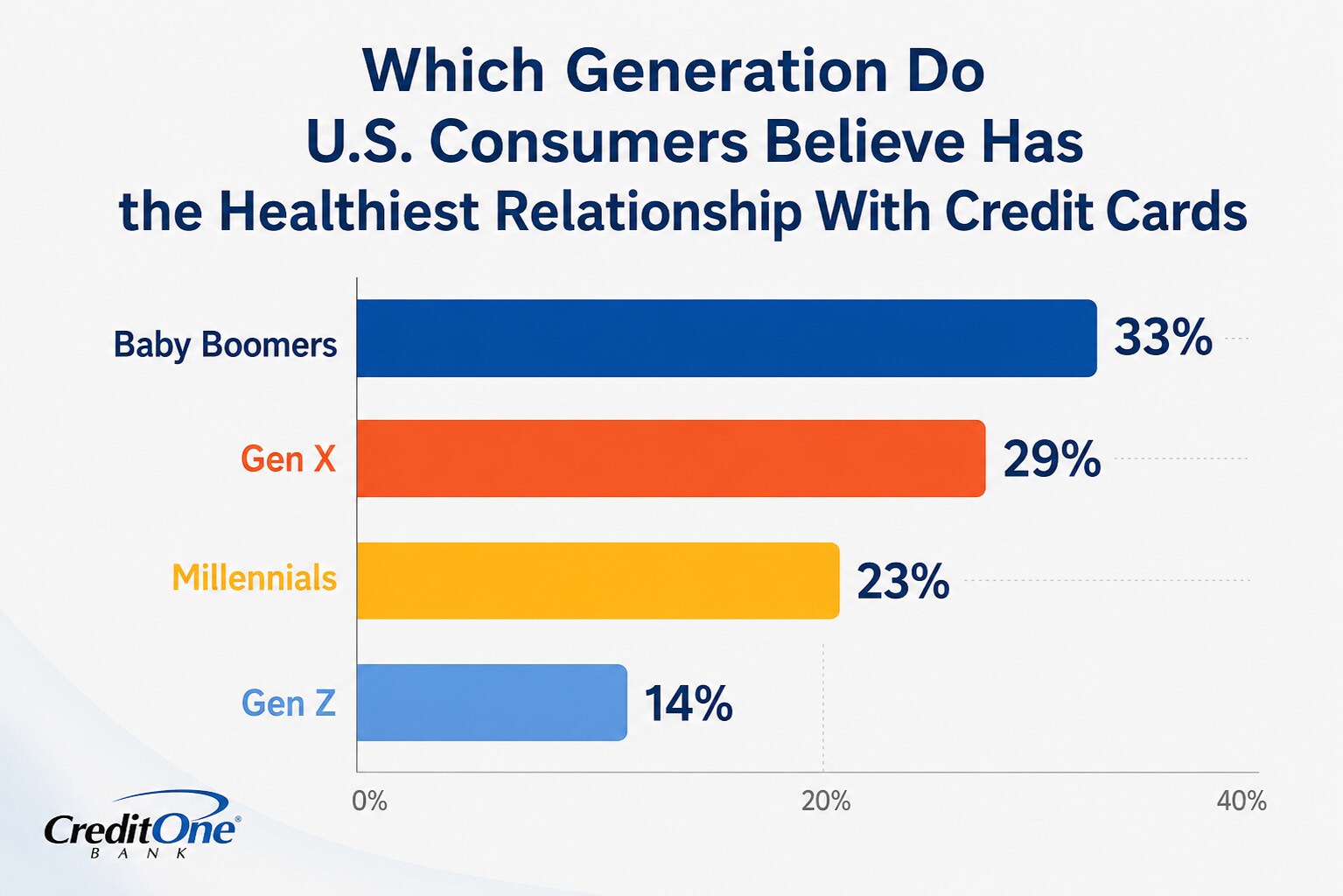

When asked which generation has the healthiest relationship with credit cards, 33% of U.S. consumers pointed to baby boomers. Gen X came in second at 29%, millennials at 23%, and Gen Z at 14%.

The perception tracks with behavior. Boomers had the lowest rate of carrying a balance (37%) and years of experience managing credit. The public sees stability in their habits, even as younger generations bring new approaches and tools to the table. Gen Z’s focus on credit-building and financial education could reshape these rankings in the years ahead.

The credit card may no longer be a one-size-fits-all product, and the data from this survey makes that clear. A 22-year-old building credit for the first time may have fundamentally different needs than a 55-year-old optimizing travel rewards. The tools they use are different, the emotions they bring to their credit relationships are different, and the way they want to learn about credit is different.

Card issuers that treat all cardholders the same could miss the generational currents shaping consumer behavior today. For Gen Z, a credit card is an investment in their financial future. For boomers and high earners, it’s a return on their financial present.

Both perspectives may be valid, and both deserve products designed around them. The companies that understand this distinction may earn the trust and long-term loyalty of the next generation of cardholders.

Find the full survey and responses here.

To understand how U.S. consumers approach credit card usage across generations, Credit One Bank surveyed 1,000 adults across the country who currently hold at least one personal credit card. Participants answered a series of questions about their credit card habits, reward preferences, payment behaviors, attitudes toward AI in personal finance, and views on financial education. Responses were analyzed by demographic groups to identify trends and disparities. Generational cohorts referenced in this article are Gen Z (ages 18 to 28), millennials (ages 29 to 44), Gen X (ages 44 to 60), and baby boomers (ages 61 to 78).

Readers are welcome to utilize the insights and findings from this study for non-commercial purposes, such as academic research, educational presentations, and personal reference. When referencing or citing this article, please ensure proper attribution to maintain the integrity of the research. Direct linking to this article is permissible, and access to the original source of information is encouraged.

For commercial use or publication purposes, including but not limited to media outlets, websites, and promotional materials, please contact the authors for permission and licensing details. We appreciate your respect for intellectual property rights and adherence to ethical citation practices. Thank you for your interest in our research.

This material is for informational purposes only and is not intended to replace the advice of a qualified tax advisor, attorney or financial advisor. Readers should consult with their own tax advisor, attorney or financial advisor with regard to their personal situations.

Tue Apr 21 2026

Poor credit can lead to denials, and that may lead to even more complications. Not all of them are what you’d expect.

Mon Dec 08 2025

Many people think they know a lot about credit. But as it turns out, there may be some crucial knowledge gaps among consumers.

Mon Oct 20 2025

What’s in a number? Find out how adults from two distinct generations factor in credit scores and financial habits as they assess relationships.