Mon Oct 14 2024

Credit Score Ranges

Your credit score range affects everything when you’re applying for credit. Learn what they mean and where you stand.

FDIC-Insured - Backed by the full faith and credit of the U.S. Government

Author: Sean P. Egen

January 17, 2022

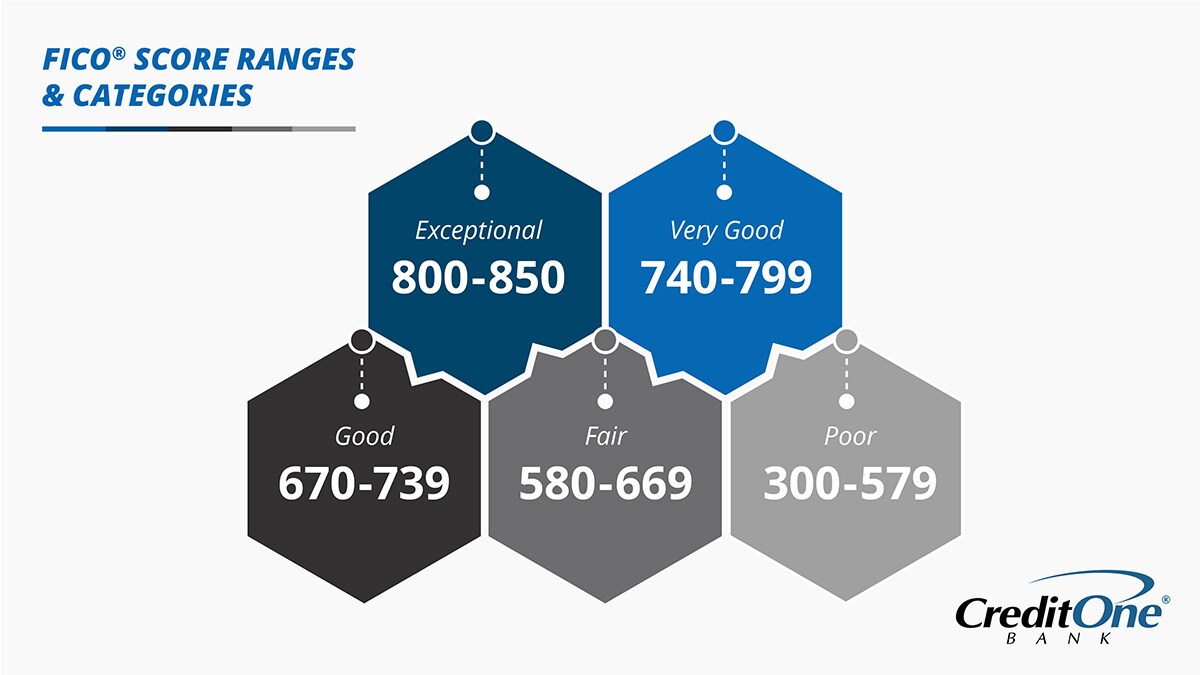

Credit scores—three-digit numbers used by lenders to help convey a consumer’s creditworthiness—range anywhere from 300 to 850 points. Within this range are sub-ranges described by one- or two-word ratings, and “Good” is one of these ratings.

A credit score of around 700 points is generally considered good; however, whether a credit score literally falls into the “Good” category depends on which consumer scoring model you’re using: FICO® Score or VantageScore®.

Any score in the 670-739 range of FICO’s credit-scoring model is considered “Good,” one of the five ratings used by FICO. This scoring model was introduced by the Fair Isaac Corporation in 1989 and is used by 90% of the top lenders.1

With the FICO scoring model, a credit score below the 670-point minimum of its Good category falls into one of two categories: “Fair” or “Poor.” A score of 580 to 669 is considered Fair, while a score of 300 to 579 qualifies as Poor. If you have a credit score that resides in either of these two categories, you likely won’t qualify for many of the same credit opportunities that require at least a Good score.

On the other end of the spectrum, a credit score greater than the 739-point maximum of FICO’s Good category falls into either their “Very Good” or “Exceptional” category. A score of 740 to 799 is considered Very Good, while a score of 800 to 850 qualifies as Exceptional. A credit score in either of these two categories should qualify you for most credit opportunities requiring at least a Good score and will likely open doors for lower interest rates, higher credit limits, more lucrative credit card rewards, lower or no fees, and other more favorable terms than you may be offered with merely a Good score.

As of April 2021, the average FICO Score for an American consumer was 716, which falls squarely within FICO’s “Good” range.2

A “Good” VantageScore, one of the five ratings used by this model, is any score falling within their 661-780 range. VantageScore was introduced in 2006 and is a joint venture of the three major credit bureaus—Experian®, Equifax®, and TransUnion®—but is managed by VantageScore Solutions, an independent company.

With VantageScore, any score below the 661-point lower limit of its Good category falls into one of three categories (unlike two with FICO Score): “Fair,” “Poor,” or “Very Poor.” A score of 601 to 660 is considered Fair, while any score falling into the 500-600 range is considered Poor. Any score between 300 and 499 falls into the bottom category of Very Poor. If you have a credit score residing in any of these lower ranges, you are not likely to qualify for credit that requires a minimum of a Good score.

Whereas FICO Score has two categories above their Good category, VantageScore has only one: “Excellent.” Any score above the 780-point upper limit of VantageScore’s Good category qualifies as Excellent. An Excellent VantageScore is likely to qualify you for most credit requiring a minimum of a Good score, plus additional credit opportunities, better perks, higher credit limits, and more advantageous interest rates and terms.

As of July 2021, the average VantageScore in America was 697, which resides in VantageScore’s “Good” range.3

If you’re applying for credit, the range and category your FICO Score or VantageScore falls within could affect you in the following ways:

Having a good credit score offers plenty of advantages with no real downside. By following these tips, you should be able to push your FICO Score and VantageScore into the “Good” category or even higher!

SOURCES

About the author:

Sean P. EgenAfter realizing he couldn’t pay back his outrageous film school student loans with rejection notices from Hollywood studios, Sean focused his screenwriting skills on scripting corporate videos. Videos led to marketing communications, which led to articles and, before he knew it, Sean was making a living as a writer. He continues to do so today by leveraging his expertise in credit, financial planning, wealth-building, and living your best life for Credit One Bank.

Mon Oct 14 2024

Your credit score range affects everything when you’re applying for credit. Learn what they mean and where you stand.

Fri Mar 08 2019

If you’ve ever applied for a loan or credit card, you probably know that lenders review your credit history and scores to help determine whether to approve you for a loan and which

Thu Oct 31 2019

They say with age comes wisdom. But does that include credit wisdom that could result in a higher credit score? Check out the average credit score by age group in the U.S.A. in this